Cryptocurrency Arbitrage (2): Performance

2018-01-09

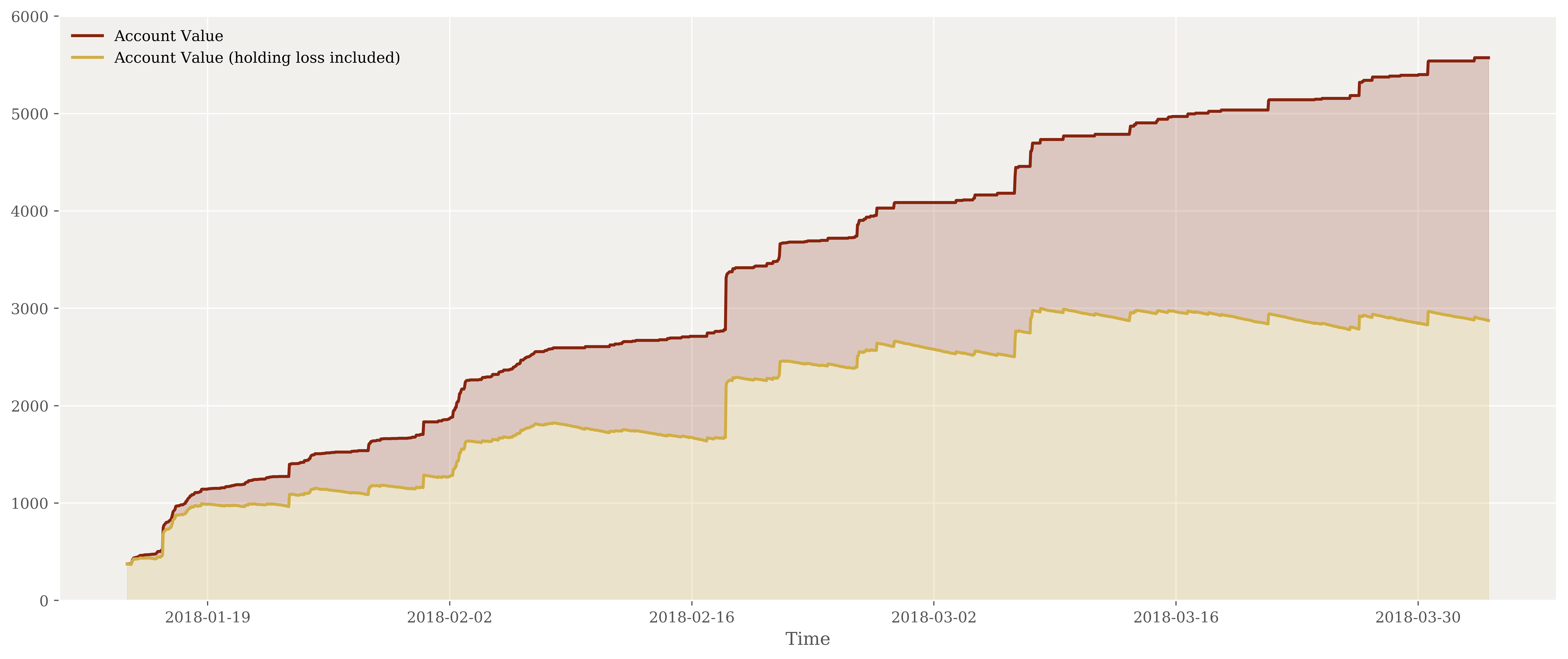

Below is the PnL plot of the multi-coin arb strategy. The strategy is running on Amazon EC2 and portfolio value pulled dynamically to plot this using plotly. Timezone is set at my local time, i.e. Europe/Amsterdam. Cheers!

Update April 11:

Strategy offline before I realized my AWS bills was being owed and the server down due to that… Performance excl. and incl. loss due to holding costs and enforcing execution, etc. (which I would call “true performance” but is actually summarized from two accounts) is compared below.

| Gross Performance | Adjusted Performance | |

|---|---|---|

| Timespan in Days | 78.72 | 78.72 |

| Cumulative Returns | +1386.17% | +651.53% |

| Annualized Returns | +6431.49% | +3022.94% |

| Sharpe Ratio | 7.35 | 7.06 |

| Maximum Drawdown | - | 8.05% |

Update June 3:

Since the mass slump this January, the strategy has experienced a remarkable decline in performance. Could be due to market panic and the corresponding flooding. Now that it’s no longer profitable, I’m sharing part of codes in the main file as below. Feel free to tell me your suggestions in comments!

# Author: Allen Frostline / Version 0.1.8

#

# - Dynamic slippage proportional to spreads

# - Order retry

# - Flush all orders and errors

# - Added a new order delay/timeout mechanism

# - Using limit order instead of market order now

# - Added a log-t estimation of expected time to a hit

# - Added the sim trading feature

# - Keep 10% BNB in the account so that fee = 5bps

import os

import imp

import sys

import ccxt

import config

import numpy as np

import pandas as pd

from time import sleep

from pytz import timezone

from scipy.stats import t

from scipy.misc import imread

from datetime import datetime

from skimage.transform import resize

VERSION = '0.1.8'

SCREEN_WIDTH = 100

PRINT_BRAND = False

if sys.stdout.isatty():

RED = '\u001b[1m\u001b[38;5;196m'

GRAY = '\u001b[1m\u001b[38;5;240m'

GREEN = '\u001b[1m\u001b[38;5;46m'

YELLOW = '\u001b[1m\u001b[38;5;220m'

CYAN = '\u001b[1m\u001b[38;5;51m'

RESET = '\u001b[0m'

else:

RED = GRAY = GREEN = YELLOW = CYAN = RESET = ''

IS_OSX = (sys.platform == 'darwin')

def now():

return datetime.now(timezone('Europe/Amsterdam'))

def log(s, flush=False):

print(' ' * (SCREEN_WIDTH + 60), end='\r')

sys.stdout.flush()

if not flush:

print('[' + GREEN + now().strftime('%Y-%m-%d %H:%M:%S') + RESET + ']', s)

else:

print('[' + GREEN + now().strftime('%Y-%m-%d %H:%M:%S') + RESET + ']', s, end='\r')

sys.stdout.flush()

YEAR = now().year

FLUSH_ORDERS = True

FLUSH_ERRORS = True

PRINT_BNB_RATIO = False

ORDER_DELAY_MAX = 1000

ORDER_RETRY_MAX = 10

HISTORY_LENGTH = 100

ERROR_LENGTH = 123

class Coinbot:

def __init__(self):

self.mtime_config = 0

self.sim_pnl = 0

self.mv0 = None

self.seconds = []

self.log_retns = []

self.init = PRINT_BRAND

def mv(self):

if self.sim:

base_amount = self.sim_amount * (1 + self.sim_pnl)

return self.mv_in_usd(self.base_coin, base_amount), base_amount

orders_made, balance = self.close_all()

if orders_made: balance = self.exchange.fetch_total_balance()

tot_mv = sum([self.mv_in_usd(c, balance[c]) for c in balance])

bnb_ratio = self.mv_in_usd('BNB', balance['BNB']) / tot_mv

return tot_mv, balance[self.base_coin], bnb_ratio

def mv_in_usd(self, c, amount):

if not amount: return 0

if c not in self.coin_list: return 0

ret = 0

rates = {'USDT': 1,

'BTC': self.tickers['BTC/USDT']['last'],

'ETH': self.tickers['ETH/USDT']['last'],

'BNB': self.tickers['BNB/USDT']['last']}

if c in rates: ret = amount * rates[c]

else:

for coin in rates:

symbol = c + '/' + coin

if symbol in self.symbols:

ret = amount * self.tickers[symbol]['last'] * rates[coin]

break

return ret * (ret > 1)

def update_config(self):

return # instructions to print good-looking configurations

def order(self, from_coin, to_coin, from_amount=None, rate=None, retry=0):

if retry > ORDER_RETRY_MAX: return False

from_amount_init = from_amount

try:

if not from_amount:

if from_coin == 'BNB':

from_amount = self.exchange.fetch_total_balance()[from_coin] * (1 - self.bnb_ratio)

else: from_amount = self.exchange.fetch_total_balance()[from_coin]

symbol = from_coin + '/' + to_coin

if symbol in self.symbols:

limit = self.limit[symbol]

from_amount = from_amount // limit * limit

if not self.mv_in_usd(from_coin, from_amount): return False

if rate:

log('Sell {:.6f} {} for {} at {:.6f} {}/{}'.

format(from_amount, from_coin, to_coin, rate, to_coin, from_coin), FLUSH_ORDERS)

self.exchange.create_limit_sell_order(symbol, from_amount, rate)

order_delay = 0

while order_delay < ORDER_DELAY_MAX:

open_orders = self.exchange.fetch_open_orders(symbol)

if open_orders:

sleep(.1)

order_delay += 1

log('Sell {:.6f} {} for {} at {:.6f} {}/{} (delay {}/{})'.

format(from_amount, from_coin, to_coin, rate, to_coin,

from_coin, order_delay, ORDER_DELAY_MAX), True)

else:

return True

for open_order in open_orders: self.exchange.cancel_order(open_order['id'], symbol)

return False

else:

log('Sell {:.6f} {} for {}'.format(from_amount, from_coin, to_coin), FLUSH_ORDERS)

self.exchange.create_market_sell_order(symbol, from_amount)

return True

else:

symbol = to_coin + '/' + from_coin

if rate:

to_amount = from_amount / rate

limit = self.limit[symbol]

to_amount = to_amount // limit * limit

if not self.mv_in_usd(to_coin, to_amount): return False

log('Buy {:.6f} {} with {} at {:.6f} {}/{}'.

format(to_amount, to_coin, from_coin, rate, from_coin, to_coin), FLUSH_ORDERS)

self.exchange.create_limit_buy_order(symbol, to_amount, rate)

order_delay = 0

while order_delay < ORDER_DELAY_MAX:

open_orders = self.exchange.fetch_open_orders(symbol)

if open_orders:

sleep(.1)

order_delay += 1

log('Buy {:.6f} {} with {} at {:.6f} {}/{} (delay {}/{})'.

format(to_amount, to_coin, from_coin, rate, from_coin, to_coin,

order_delay, ORDER_DELAY_MAX), True)

else:

return True

for open_order in open_orders: self.exchange.cancel_order(open_order['id'], symbol)

return False

else:

to_amount = 0

order_book = self.exchange.fetch_order_book(symbol)

slippage = self.updated_slippage(symbol, order_book)

for x in order_book['asks']:

p = x[0] * (1 + slippage)

a = x[1]

if a * p < from_amount:

to_amount += a

from_amount -= a * p

else:

to_amount += from_amount / p

from_amount -= from_amount

break

limit = self.limit[symbol]

to_amount = to_amount // limit * limit

if not self.mv_in_usd(to_coin, to_amount): return False

log('Buy {:.6f} {} with {}'.format(to_amount, to_coin, from_coin), FLUSH_ORDERS)

self.exchange.create_market_buy_order(symbol, to_amount)

return True

except AssertionError:

raise

except Exception as e:

if IS_OSX: os.system('afplay /System/Library/Sounds/Hero.aiff')

err = str(e)

log('Error: {}...'.format(err[:ERROR_LENGTH].strip()), FLUSH_ERRORS)

if symbol:

open_orders = self.exchange.fetch_open_orders(symbol)

for open_order in open_orders: self.exchange.cancel_order(open_order['id'], symbol)

else:

sleep(.1)

self.order(from_coin, to_coin, from_amount=from_amount_init, rate=rate, retry=retry + 1)

def close_all(self):

orders_made = False

balance = self.exchange.fetch_total_balance()

# all to btc (except bnb, usdt and btc)

for c in balance:

if not self.mv_in_usd(c, balance[c]): continue

if c in [self.base_coin, 'BNB', 'BTC']: continue

orders_made += self.order(c, 'BTC')

# all BTC -> BASE_COIN

if self.base_coin != 'BTC': orders_made += self.order('BTC', self.base_coin)

# if BASE_COIN is not BNB

if self.base_coin != 'BNB':

# calc ratio of bnb (both in usd)

tot_mv = sum([self.mv_in_usd(c, balance[c]) for c in balance])

bnb_mv = self.mv_in_usd('BNB', balance['BNB'])

bnb_ratio = round(bnb_mv / tot_mv * 100) / 100

# calc offset and make orders BASE_COIN -> BNB

bnb_usdt = self.tickers['BNB/USDT']['last']

base_usdt = self.tickers[self.base_coin + '/USDT']['last'] if self.base_coin != 'USDT' else 1

if bnb_ratio > self.bnb_ratio:

orders_made += self.order('BNB', self.base_coin,

from_amount=tot_mv * (bnb_ratio - self.bnb_ratio) / bnb_usdt)

elif bnb_ratio < self.bnb_ratio:

orders_made += self.order(self.base_coin, 'BNB',

from_amount=tot_mv * (self.bnb_ratio - bnb_ratio) / base_usdt)

return orders_made, balance

def simulate(self, path):

from_coin = path[-1]

ffrom_coin = None if len(path) == 1 else path[-2]

path_list = []

for symbol in self.symbols:

ss = symbol.split('/')

if (from_coin not in ss) or (ffrom_coin in ss): continue

to_coin = ss[1] if from_coin == ss[0] else ss[0]

if to_coin == self.base_coin: path_list.append(path + [to_coin])

elif len(path) < self.max_len - 1:

temp = self.simulate(path + [to_coin])

if not temp: continue

else: path_list += temp

return path_list

def updated_slippage(self, symbol, order_book):

spread = (order_book['asks'][0][0] - order_book['bids'][0][0]) / order_book['asks'][0][0]

self.spreads[symbol].append(spread)

if len(self.spreads) > HISTORY_LENGTH: self.spreads.pop(0)

mean_spread = np.mean(self.spreads[symbol])

return mean_spread * self.slippage_ratio

def optimum(self, base_amount):

return path, ratio, amount # MCTS algorithm

def cancel_all(self):

log('Cancelling all open orders', True)

for symbol in self.symbols:

open_orders = self.exchange.fetch_open_orders(symbol)

if open_orders:

for open_order in open_orders:

self.exchange.cancel_order(open_order['id'], open_order['symbol'])

def trade(self):

self.tickers = self.exchange.fetch_tickers(self.symbols)

self.order_book = {symbol: self.exchange.fetch_order_book(symbol) for symbol in self.symbols}

mv, base_amount, bnb_ratio = self.mv()

opt = self.optimum(base_amount)

if opt is None: return False

opt_path, opt_retn, opt_rate_list = opt

self.end = now()

self.seconds.append((self.end - self.start).seconds)

self.log_retns.append(np.log(1 + opt_retn))

if len(self.seconds) > HISTORY_LENGTH:

self.seconds.pop(0)

self.log_retns.pop(0)

freq = 60 / np.mean(self.seconds)

if len(self.seconds) > 5:

ccdf = 1 - t.cdf(self.threshold, *t.fit(self.log_retns))

if ccdf > 1e-4: exp_rounds = 1 / ccdf

else: exp_rounds = np.inf

else: exp_rounds = np.inf

len_trans = len(opt_path) - 1

mv_str = '$' + RED + '{:.4f}'.format(mv) + RESET + '/' + \

RED + '{:+.4f}'.format(mv / self.mv0 * 100 - 100) + RESET + '% '

path_str = '[' + ' \u2192 '.join([YELLOW + coin + RESET for coin in opt_path]) + '] '

retn_str = CYAN + '{:+.4f}'.format(opt_retn * 10000) + RESET + 'bps '

freq_str = '(' + GREEN + '{:.2f}'.format(freq) + RESET + 'rpm/' + \

GREEN + '{:.2f}'.format(exp_rounds / freq) + RESET + 'mph)'

log_str = mv_str + path_str + retn_str + freq_str

if PRINT_BNB_RATIO:

ratio_str = ' ~ {:.2f}%'.format(bnb_ratio * 100)

log_str += ratio_str

log(log_str, True)

if (opt_retn > self.threshold):

log(log_str)

if IS_OSX: os.system('afplay /System/Library/Sounds/Ping.aiff')

if self.sim:

self.sim_pnl += (1 + self.sim_pnl) * opt_retn

else:

for i in range(len_trans):

from_coin = opt_path[i]

to_coin = opt_path[i + 1]

rate = opt_rate_list[i]

order_result = self.order(from_coin, to_coin, rate=rate)

if order_result is False:

log('Order cancelled', True)

break

if IS_OSX: os.system('afplay /System/Library/Sounds/Tink.aiff')

self.start = now()

def run(self):

try:

while True:

mtime_config = os.path.getmtime('config.py')

if mtime_config != self.mtime_config: self.update_config()

self.trade()

self.mtime_config = mtime_config

except KeyboardInterrupt:

self.cancel_all()

log('Good bye')

except (AssertionError, KeyError) as e:

if IS_OSX: os.system('afplay /System/Library/Sounds/Hero.aiff')

err = str(e)

log(err, FLUSH_ERRORS)

sleep(.1)

self.cancel_all()

self.start = now()

self.run()

except Exception as e:

if IS_OSX: os.system('afplay /System/Library/Sounds/Hero.aiff')

err = str(e)

if 'until' in err:

idx = err.index('until') + 6

timestamp = int(err[idx: idx + 13])

wait = (datetime.fromtimestamp(timestamp / 1000) - datetime.now()).seconds

for i in range(wait):

log('Error: too many requests, IP banned for {} seconds'.format(wait - i), True)

sleep(1)

else:

log('Error: {}...'.format(err[:ERROR_LENGTH].strip()), FLUSH_ERRORS)

sleep(.1)

self.cancel_all()

self.start = now()

self.run()

if __name__ == '__main__':

agent = Coinbot()

agent.run()