Basic Walkthrough of ARMA: Take AAPL for Example

2017-03-11

The ARMA model consists of two parts: Auto-Regressive and Moving Average. This is a powerful tool in predicting stationary time series. Today, we’re going to apply it on the stock price of Apple Inc. We will perform the prediction mainly in four parts:

- Data loading

- Decomposition

- ARMA: fit and predict

- Evaluation

After the whole process, there’re some TBD concerns.

Data loading

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from yahoo_finance import Share

from datetime import datetime

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.stattools import adfuller, acf, pacf, arma_order_select_ic

from statsmodels.tsa.arima_model import ARMA, _arma_predict_out_of_sample

np.random.seed(123) # fix random seed for reproducibility

pd.set_option('display.width', 1000)

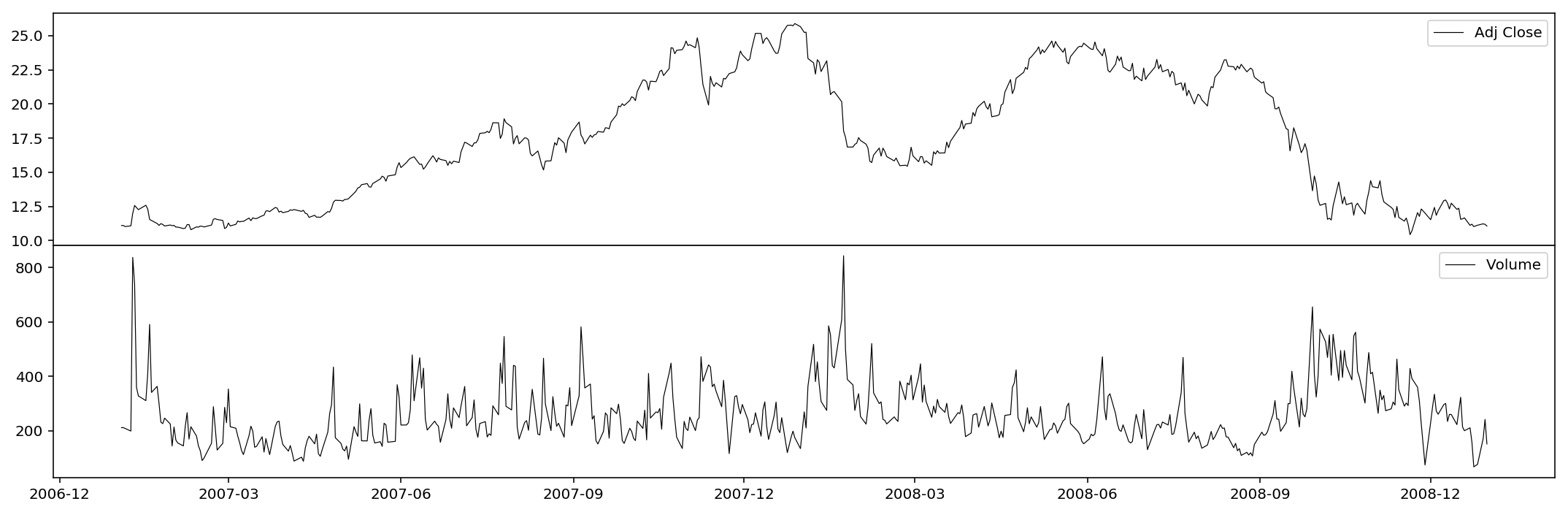

Here we extract the historical data of AAPL from 2007-01-01 to 2009-01-01, which exactly covers the explosion of 2008 subprime crisis. We only consider adjusted close prices and volumes.

# load the dataset

start = '2007-01-01'

end = '2009-01-01'

AAPL = Share('AAPL')

historical = AAPL.get_historical(start_date=start, end_date=end)

df = pd.DataFrame(historical).ix[::-1,['Date','Adj_Close','Volume']]

df = df.set_index('Date').astype(np.float64)

df.index = pd.to_datetime(df.index)

df.Volume /= 1e6 # volume in millions

df.ix[0,:] = df.ix[1,:]

print(df.tail())

print(df.dtypes)

Adj_Close Volume

Date

2008-12-24 11.017744 67.8335

2008-12-26 11.117505 77.0812

2008-12-29 11.221153 171.5000

2008-12-30 11.179694 241.9004

2008-12-31 11.057907 151.8853

Adj_Close float64

Volume float64

dtype: object

As you can see, I here devide the volume by some properly large number so that the scales of the variables are similar.

print(df.describe())

Adj_Close Volume

count 504.000000 504.000000

mean 17.510924 264.179629

std 4.551519 111.138634

min 10.428248 67.833500

25% 12.748336 188.703025

50% 17.160162 240.869300

75% 21.891029 308.259350

max 25.889884 843.242400

%config InlineBackend.figure_format = 'retina'

plt.figure(figsize=(15,5))

ax1 = plt.subplot2grid((2,1), (0,0))

ax1.plot(df.Adj_Close, lw=0.6, color='k')

ax1.set_xlabel('')

ax1.get_xaxis().set_visible(False)

ax1.legend(['Adj Close'])

ax2 = plt.subplot2grid((2,1), (1,0))

ax2.plot(df.Volume, lw=0.6, color='k')

ax2.legend(['Volume'])

plt.tight_layout()

plt.subplots_adjust(hspace=0)

plt.show()

Decomposition

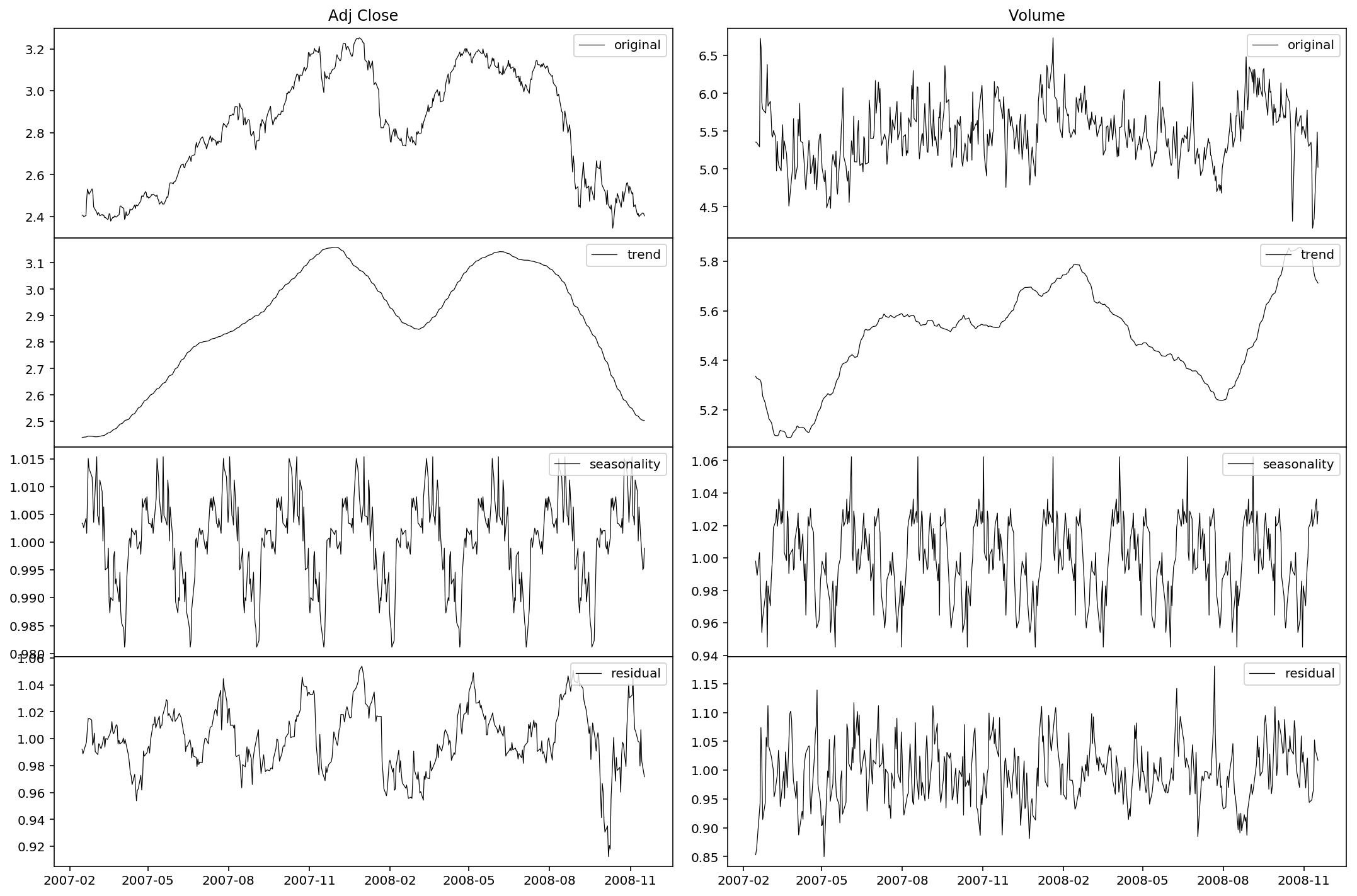

First we take the logarithm of the series. This is totally reversible and in many cases w.r.t. time series could efficiently improve the stationarity.

df = np.log(df)

Then we decompose the series by three parts: trend, seasonality and residual.

dec_Adj_Close = seasonal_decompose(df.Adj_Close, model='multiplicative', freq=60)

dec_Volume = seasonal_decompose(df.Volume, model='multiplicative', freq=60)

The charts are plotted below.

%config InlineBackend.figure_format = 'retina'

plt.figure(figsize=(15,10))

ax1 = plt.subplot2grid((4,2), (0,0))

ax1.plot(df.Adj_Close, lw=0.6, color='k')

ax1.get_xaxis().set_visible(False)

ax1.legend(['original'], loc='upper right')

ax1.set_title('Adj Close')

ax2 = plt.subplot2grid((4,2), (1,0))

ax2.plot(dec_Adj_Close.trend, lw=0.6, color='k')

ax2.get_xaxis().set_visible(False)

ax2.legend(['trend'], loc='upper right')

ax3 = plt.subplot2grid((4,2), (2,0))

ax3.plot(dec_Adj_Close.seasonal, lw=0.6, color='k')

ax3.get_xaxis().set_visible(False)

ax3.legend(['seasonality'], loc='upper right')

ax4 = plt.subplot2grid((4,2), (3,0))

ax4.plot(dec_Adj_Close.resid, lw=0.6, color='k')

ax4.legend(['residual'], loc='upper right')

ax5 = plt.subplot2grid((4,2), (0,1))

ax5.plot(df.Volume, lw=0.6, color='k')

ax5.get_xaxis().set_visible(False)

ax5.legend(['original'], loc='upper right')

ax5.set_title('Volume')

ax6 = plt.subplot2grid((4,2), (1,1))

ax6.plot(dec_Volume.trend, lw=0.6, color='k')

ax6.get_xaxis().set_visible(False)

ax6.legend(['trend'], loc='upper right')

ax7 = plt.subplot2grid((4,2), (2,1))

ax7.plot(dec_Volume.seasonal, lw=0.6, color='k')

ax7.get_xaxis().set_visible(False)

ax7.legend(['seasonality'], loc='upper right')

ax8 = plt.subplot2grid((4,2), (3,1))

ax8.plot(dec_Volume.resid, lw=0.6, color='k')

ax8.legend(['residual'], loc='upper right')

plt.tight_layout()

plt.subplots_adjust(hspace=0)

plt.show()

As we can see, the seasonality is periodically significant. Also we may notice the trend behavior in late 2008: a continuous slump in the price and a lagged surge in the volume. The market panic is well illustrated. It’s sure that the seasonality is stationary, but as for the residual, it remains to be tested. Now let’s define a function to test the stationarity of the residuals. We use the Dickey-Fuller test to examine the existence of a unit root.

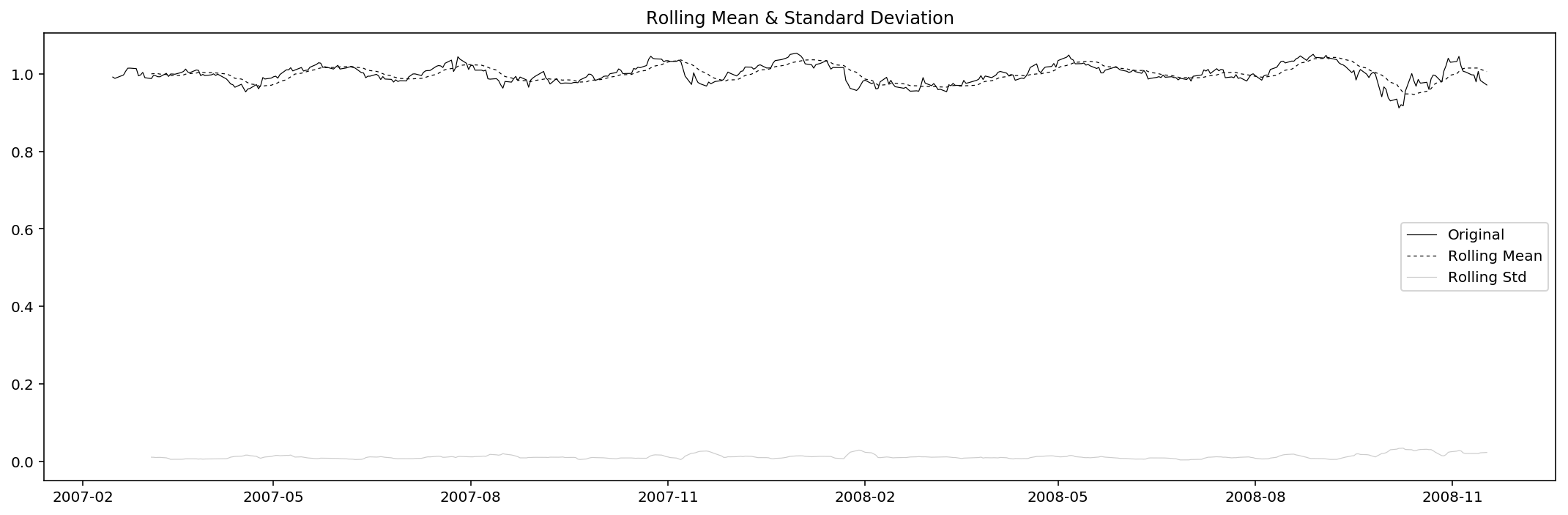

%config InlineBackend.figure_format = 'retina'

def test_stationarity(timeseries):

#Determing rolling statistics

rolmean = timeseries.rolling(center=False, window=12).mean()

rolstd = timeseries.rolling(center=False, window=12).std()

#Plot rolling statistics:

plt.figure(figsize=(15,5))

orig = plt.plot(timeseries, 'k-', lw=0.6, label='Original')

mean = plt.plot(rolmean, 'k:', lw=0.6, label='Rolling Mean')

std = plt.plot(rolstd, 'k-', alpha=0.2, lw=0.6, label = 'Rolling Std')

plt.legend()

plt.title('Rolling Mean & Standard Deviation')

plt.tight_layout()

plt.show()

#Perform Dickey-Fuller test:

print('Results of Dickey-Fuller Test:')

dftest = adfuller(timeseries, autolag='AIC')

dfoutput = pd.Series(dftest[0:4], index=['Test Statistic','p-value','#Lags Used','Number of Observations Used'])

for key,value in dftest[4].items():

dfoutput['Critical Value (%s)'%key] = value

print(dfoutput)

Now let’s use our test function.

res_Adj_Close = dec_Adj_Close.resid.dropna()

test_stationarity(res_Adj_Close)

Results of Dickey-Fuller Test:

Test Statistic -5.663466e+00

p-value 9.265660e-07

#Lags Used 1.600000e+01

Number of Observations Used 4.270000e+02

Critical Value (1%) -3.445758e+00

Critical Value (5%) -2.868333e+00

Critical Value (10%) -2.570388e+00

dtype: float64

Since the test tatistic is way smaller than the 1% critical value (and the p-value also really small), we reject the null, i.e. we take it that the residual of adjusted close price is stationary under 1% significance level.

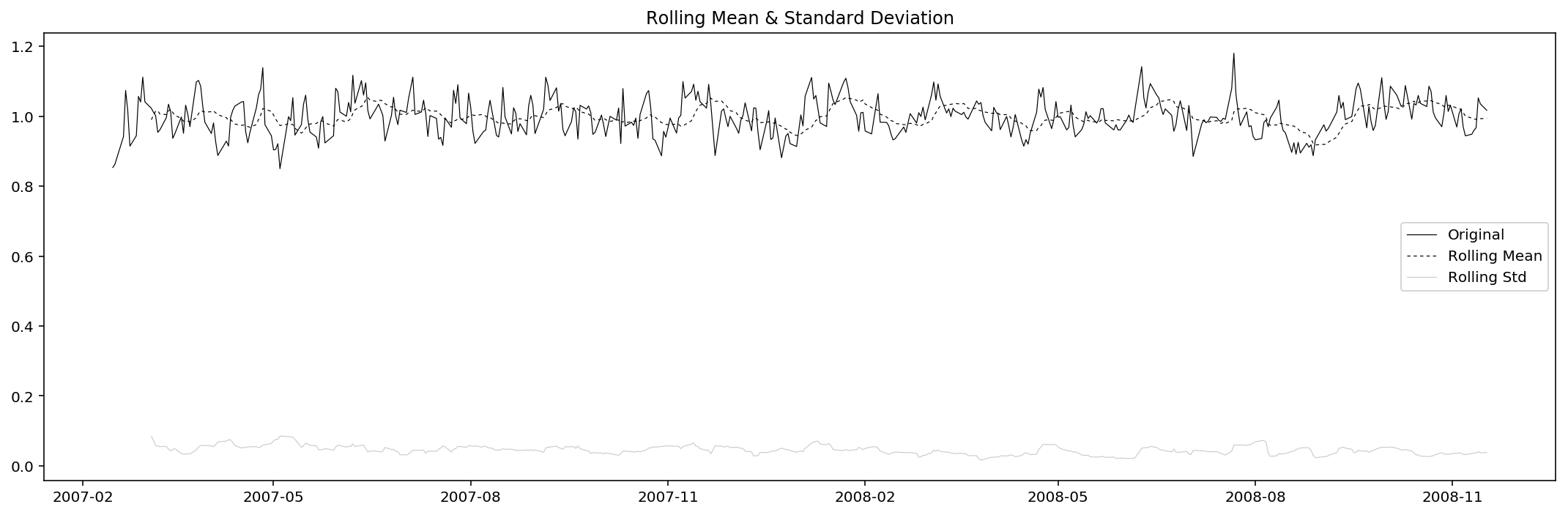

res_Volume = dec_Volume.resid.dropna()

test_stationarity(res_Volume)

Results of Dickey-Fuller Test:

Test Statistic -1.165042e+01

p-value 2.043672e-21

#Lags Used 0.000000e+00

Number of Observations Used 4.430000e+02

Critical Value (1%) -3.445198e+00

Critical Value (5%) -2.868086e+00

Critical Value (10%) -2.570257e+00

dtype: float64

Similar to that of adjusted close price, the residual of volume is considered to be stationary under 1% significance level.

ARMA: fit and predict

Now with stationary time series, we can start forecasting. There are two situations:

- A strictly stationary series with no dependence on past values.

- A series with significant dependence on past values. In this case we need to use some statistical models like ARMA to forecast the data.

Here we are of course using the latter one, and thus we need to specify the parameters of the model:

- Number of AR (Auto-Regressive) terms (

$p$): AR terms are just lags of dependent variable. For instance if$p$is$5$, the predictors for$x_t$will be$x_{t-1},x_{t-2},\ldots,x_{t-5}$. - Number of MA (Moving Average) terms (

$q$): MA terms are lagged forecast errors in prediction equation. For instance if$q$is$5$, the predictors for$x_t$will be$e_{t-1},e_{t-2},\ldots,e_{t-5}$where$e_i$is the difference between the moving average at$i^{th}$instant and actual value.

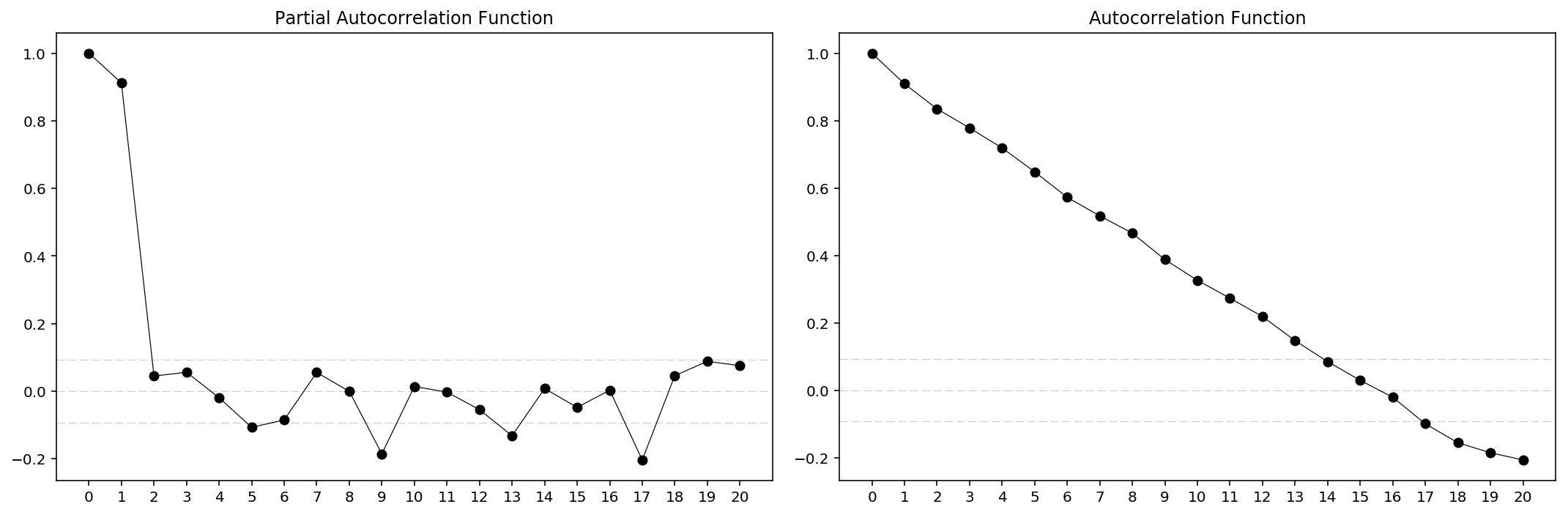

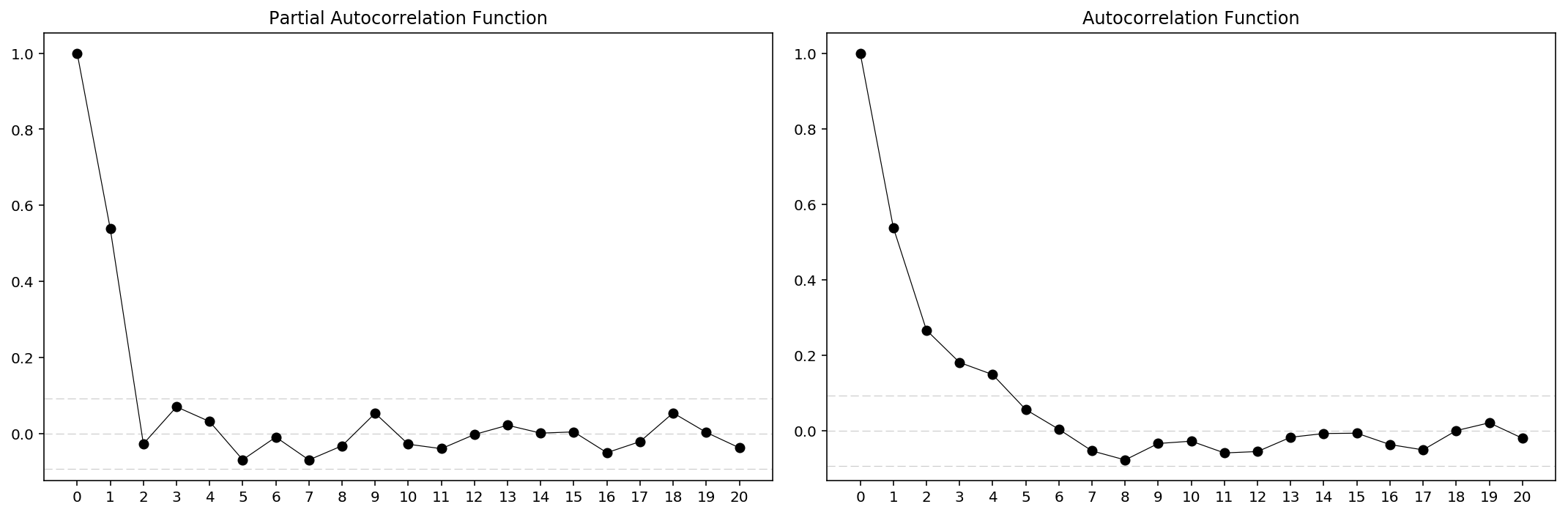

An importance concern here is how to determine the values of $p$ and $q$. Below we plot the ACF and PACF charts to determine them. The rules are:

$p$: The lag value where the PACF chart crosses the upper confidence interval for the first time.$q$: The lag value where the ACF chart crosses the upper confidence interval for the first time.

So first, let’s plot the ACF and PACF charts.

%config InlineBackend.figure_format = 'retina'

def acfplot(timeseries):

#ACF and PACF plots:

nlags = 20

#Pre-set ACF and PACF:

lag_acf = acf(timeseries, nlags=nlags)

lag_pacf = pacf(timeseries, nlags=nlags, method='ols')

fig = plt.figure(figsize=(15,5))

#Plot PACF:

ax1 = fig.add_subplot(121)

ax1.plot(lag_pacf, 'ko-', lw=0.6)

ax1.set_xticks(range(nlags+1))

ax1.axhline(y=0, ls='--', c='k', lw=0.6, alpha=0.2)

ax1.axhline(y=-1.96/np.sqrt(len(timeseries)), ls='--', c='k', lw=0.6, alpha=0.2)

ax1.axhline(y=1.96/np.sqrt(len(timeseries)), ls='--', c='k', lw=0.6, alpha=0.2)

ax1.set_title('Partial Autocorrelation Function')

#Plot ACF:

ax2 = fig.add_subplot(122)

ax2.plot(lag_acf, 'ko-', lw=0.6)

ax2.set_xticks(range(nlags+1))

ax2.axhline(y=0, ls='--', c='k', lw=0.6, alpha=0.2)

ax2.axhline(y=-1.96/np.sqrt(len(timeseries)), ls='--', c='k', lw=0.6, alpha=0.2)

ax2.axhline(y=1.96/np.sqrt(len(timeseries)), ls='--', c='k', lw=0.6, alpha=0.2)

ax2.set_title('Autocorrelation Function')

plt.tight_layout()

plt.show()

acfplot(res_Adj_Close)

acfplot(res_Volume)

From the charts it is clear that for $Adj\ Close$ we have $p=2$, $q=14$ and for $Volume$ we have $p=2$, $q=5$. Then we can load the ARIMA models for prediction. However, there’re actually built-in method for that, which is quite more direct.

order = arma_order_select_ic(res_Adj_Close, max_ar=5, max_ma=20, ic=['aic', 'bic', 'hqic'])

order.bic_min_order

/Users/Allen_Frostline/anaconda3/lib/python3.6/site-packages/statsmodels/base/model.py:466: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

/Users/Allen_Frostline/anaconda3/lib/python3.6/site-packages/statsmodels/base/model.py:466: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

...

/Users/Allen_Frostline/anaconda3/lib/python3.6/site-packages/statsmodels/base/model.py:466: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

(1, 0)

… and yes, unreliable and horribly slow. Just forget about that. Let’s continue with the ARMA model.

%config InlineBackend.figure_format = 'retina'

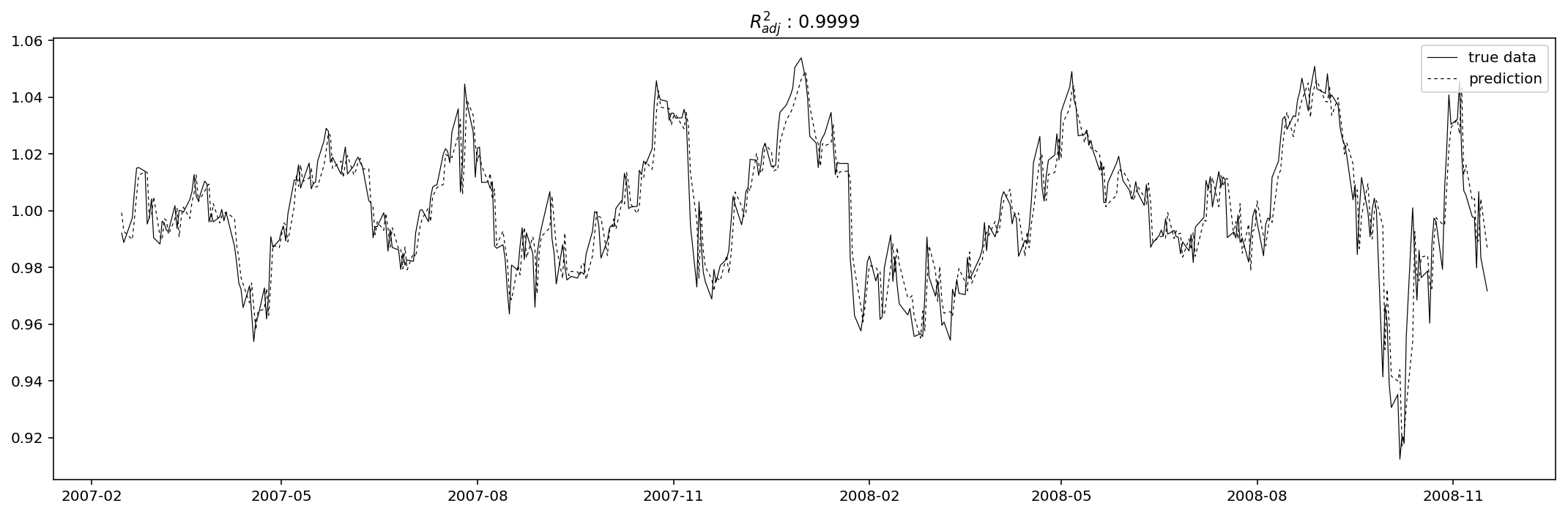

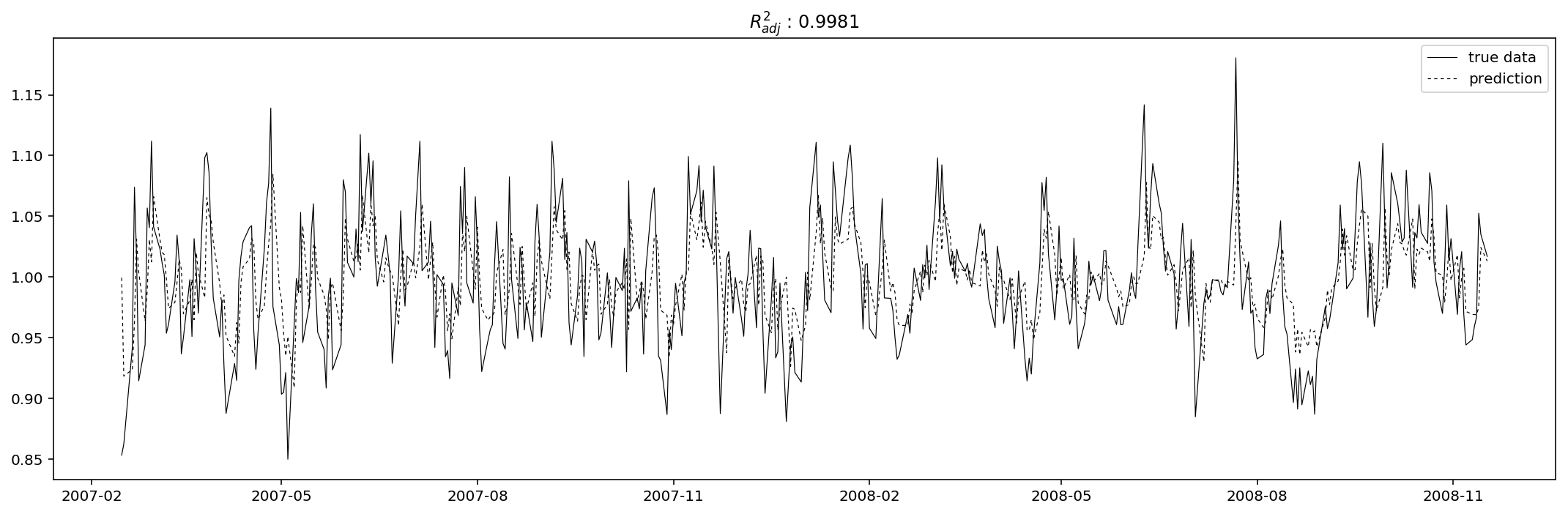

def pred(timeseries, p, q):

model = ARMA(timeseries, (p, q)).fit()

pred = model.fittedvalues

plt.close()

plt.figure(figsize=(15,5))

plt.plot(timeseries, 'k-', lw=0.6, label='true data')

plt.plot(pred, 'k:', lw=0.6, label='prediction')

plt.title('$R_{{adj}}^2$ : {:.4f}'.format(1-(sum((pred - timeseries)**2)/(len(timeseries)-p-q-1))/(sum(timeseries**2)/(len(timeseries)-1)))) # Residual Sum of Squares, RSS = SUM[(y-f(x))^2]

plt.legend(loc='upper right')

plt.tight_layout()

plt.show()

return model, pred

model_res_Adj_Close, pred_res_Adj_Close = pred(res_Adj_Close, 2, 14)

/Users/Allen_Frostline/anaconda3/lib/python3.6/site-packages/statsmodels/base/model.py:466: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

model_res_Volume, pred_res_Volume = pred(res_Volume, 2, 5)

/Users/Allen_Frostline/anaconda3/lib/python3.6/site-packages/statsmodels/base/model.py:466: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

Evaluation

Just as what I did above, I use adjusted R-square as the evaluation metric function. The “adjusted” means the R-square is punished for too many explanatory variables, and thus can in a way reduce the tendency of overfitting.

%config InlineBackend.figure_format = 'retina'

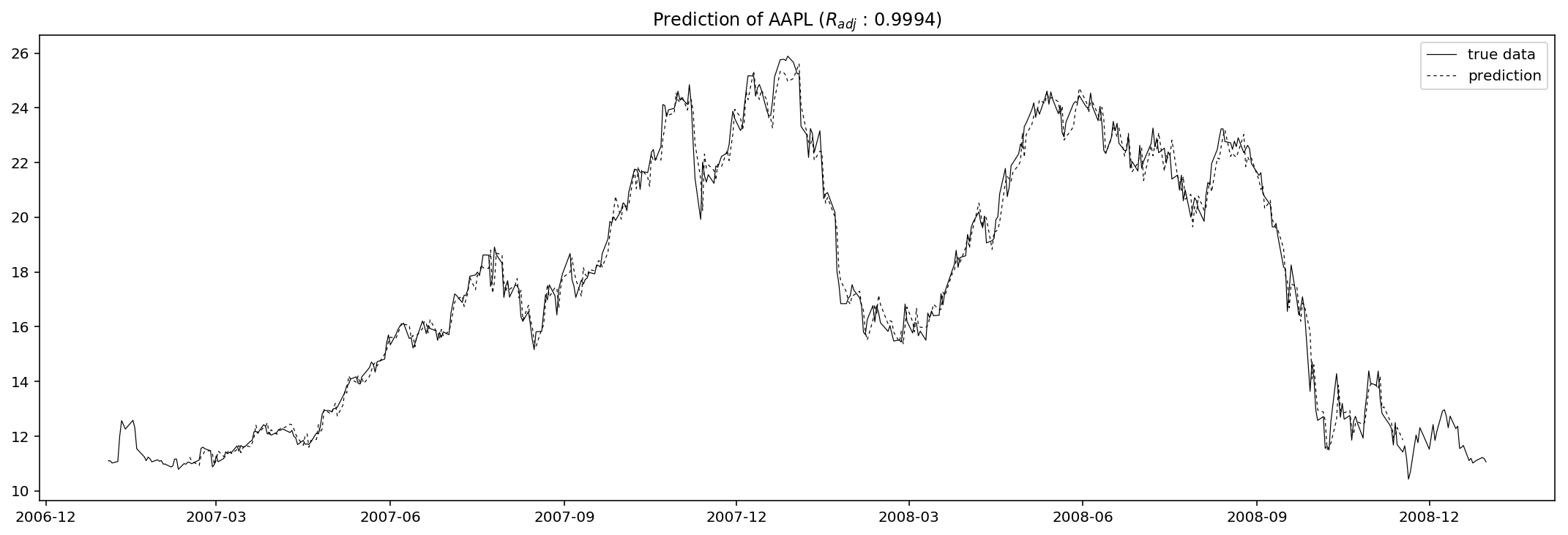

plt.figure(figsize=(15,5))

pred = dec_Adj_Close.trend * dec_Adj_Close.seasonal * pred_res_Adj_Close

data = np.exp(df.Adj_Close)

pred = np.exp(pred)

plt.plot(data, 'k-', lw=0.6, label='true data')

plt.plot(pred, 'k:', lw=0.6, label='prediction')

plt.tight_layout()

plt.legend()

plt.title('Prediction of AAPL ($R_{{adj}}$ : {:.4f})'.format(1-(sum((pred - data).dropna()**2)/(len(data)-2-14-1))/(sum(data.dropna()**2)/(len(data)-1))))

plt.show()

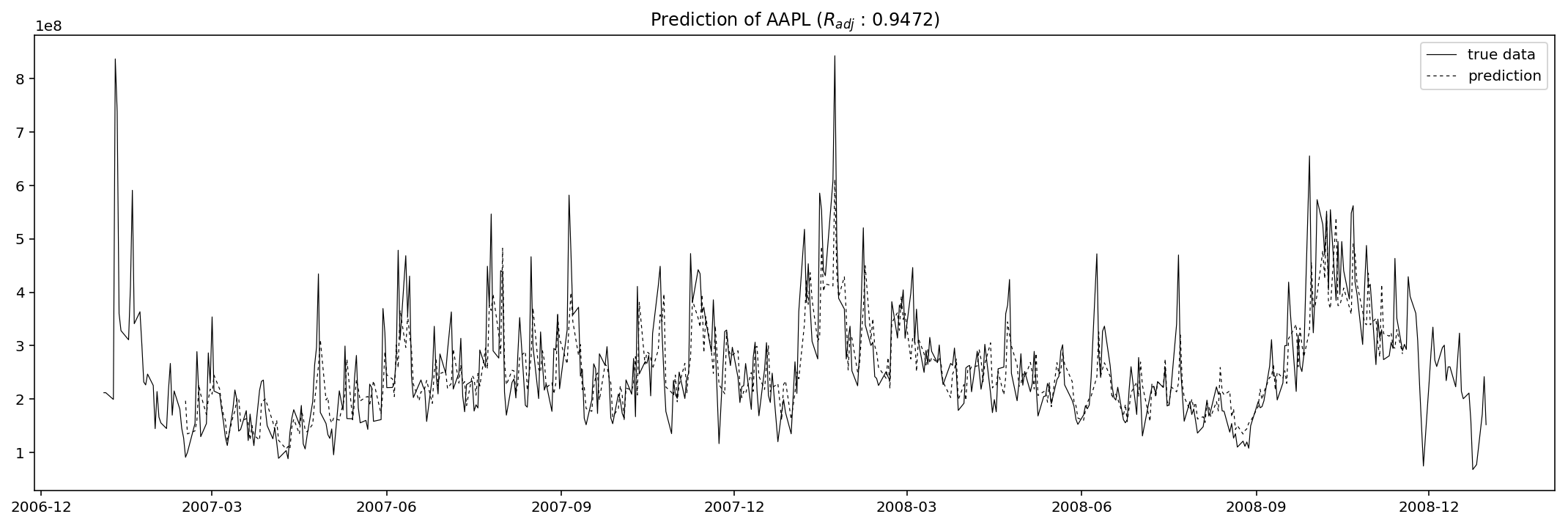

%config InlineBackend.figure_format = 'retina'

plt.figure(figsize=(15,5))

pred = dec_Volume.trend * dec_Volume.seasonal * pred_res_Volume

data = np.exp(df.Volume) * 1e6

pred = np.exp(pred) * 1e6

plt.plot(data, 'k-', lw=0.6, label='true data')

plt.plot(pred, 'k:', lw=0.6, label='prediction')

plt.tight_layout()

plt.legend()

plt.title('Prediction of AAPL ($R_{{adj}}$ : {:.4f})'.format(1-(sum((pred - data).dropna()**2)/(len(data)-2-5-1))/(sum(data.dropna()**2)/(len(data)-1))))

plt.show()

The results seem good, but never forget that this is only the in-sample prediction, so in other words this could be totally an opposite scenario when we use this fitted model to predict out-sample values, i.e. to predict the adjusted close or volume on 2009-01-02 (a Friday).

params = model_res_Adj_Close.params

residuals = model_res_Adj_Close.resid

p = model_res_Adj_Close.k_ar

q = model_res_Adj_Close.k_ma

k_exog = model_res_Adj_Close.k_exog

k_trend = model_res_Adj_Close.k_trend

steps = 5

_arma_predict_out_of_sample(params, steps, residuals, p, q, k_trend, k_exog, endog=res_Adj_Close, exog=None, start=len(res_Adj_Close)).squeeze()

array([ 0.97023813, 0.97742186, 0.97331353, 0.97333901, 0.981861 ])

params = model_res_Volume.params

residuals = model_res_Volume.resid

p = model_res_Volume.k_ar

q = model_res_Volume.k_ma

k_exog = model_res_Volume.k_exog

k_trend = model_res_Volume.k_trend

steps = 5

_arma_predict_out_of_sample(params, steps, residuals, p, q, k_trend, k_exog, endog=res_Volume, exog=None, start=len(res_Volume)).squeeze()

array([ 1.00925408, 1.01171945, 1.00450219, 0.99949544, 0.99683326])

Conclusion & concerns

Another concern is (which is really obvious), that here when back-computing the predicted values I used the formular

$$ Y_{total} = Y_{trend} \cdot Y_{seasonality} \cdot Y_{residual} $$

but only the residual is predicted using our ARMA model. The rest two parts, of cource, should also be predicted and then we can finally call it a “prediction”. Otherwise we are only partially predicting the series. For the seasonality we may directly do a translation as the patterns are very stable. However, as for the trend composition, neither translation nor ARMA are going to work well. My suggestion is to resort to deep learning or some RNN models (like LSTM in another post of mine). Machine learning in the field of time series prediction is indeed promising and stunning in recent years.

Another concern, which is actually way more important, is that we lack out-sample prediction here. This is also called cross validation. Why is cross validation so important? Because if we don’t do any cross validation, then we can always use as many explanatory variables as possible to achieve better scores in evaluation, which is most likely how overfitting happens. What we are gonna do to eliminate this, is to use historical data within time range, say, from 2009-01-01 to 2009-06-01, to predict the adjusted close prices and volumes day by day. The adjusted R-square is then the “test score” of the model, while implicitly the former R-square becomes the “train score”.

References:

- McKinney, Wes, Josef Perktold, and Skipper Seabold. “Time series analysis in Python with statsmodels.” Jarrodmillman. Com (2011): 96-102.

- Kwiatkowski, Denis, et al. “Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root?.” Journal of econometrics 54.1-3 (1992): 159-178.

- 竹间为简, “AR(I)MA时间序列建模过程”.

- Seasonal ARIMA with Python

- 有什么好的模型可以做高精度的时间序列预测呢?

- Machine Learning Strategies for Time Series Prediction

- A Youtube Course on AR, MA, ARMA and ARIMA