Literature Review on Optimal Order Execution (5)

2018-05-12

This is the fifth post on optimal order execution. Based on Almgren and Chriss (2000), today we attempt to estimate the market impact coefficient $\eta$. Specifically, for high-frequency transaction data, we have the approximation $dS = \eta\cdot dQ$ and thus can easily estimate it by the method of Ordinary Least Squares (OLS), using the message book data provided by LOBSTER.

Experiment: Apple

We first explore the message book of Apple Inc. (symbol: AAPL) from 09:30 to 16:00 on June 21, 2012.

import pandas as pd

import numpy as np

import statsmodels.formula.api as sm

import matplotlib.pyplot as plt

pd.options.mode.chained_assignment = None

According to the instructions by LOBSTER, the columns of the message book are defined as follows:

- time: seconds after midnight with decimal precision of at least milliseconds and up to nanoseconds depending on the requested period

- type:

1means submission of a new limit order;2means Cancellation (partial deletion of a limit order);3means deletion (total deletion of a limit order);4means execution a visible limit order;5means Execution of a hidden limit order;7means Trading halt indicator (detailed information below) - id: unique order reference number (assigned in order flow)

- size: number of shares

- price: dollar price times 10000 (i.e., a stock price of 91.14USD is given by 911400)

- direction:

-1means means Sell limit order;1means Buy limit order

message = pd.read_csv('data/AAPL_2012-06-21_34200000_57600000_message_1.csv', header=None)

message.columns = ['time', 'type', 'id', 'size', 'price', 'direction']

message.price /= 10000

message.head()

| time | type | id | size | price | direction | |

|---|---|---|---|---|---|---|

| 0 | 34200.004241 | 1 | 16113575 | 18 | 585.33 | 1 |

| 1 | 34200.025552 | 1 | 16120456 | 18 | 585.91 | -1 |

| 2 | 34200.201743 | 3 | 16120456 | 18 | 585.91 | -1 |

| 3 | 34200.201781 | 3 | 16120480 | 18 | 585.92 | -1 |

| 4 | 34200.205573 | 1 | 16167159 | 18 | 585.36 | 1 |

| 5 | 34200.201781 | 3 | 16120480 | 18 | 585.92 | -1 |

| 6 | 34200.205573 | 1 | 16167159 | 18 | 585.36 | 1 |

message_plce = message[message.type==1]

message_exec = message[message.type==4]

message_temp = pd.merge(message_plce, message_exec, on='id', how='inner')

message_temp.columns

Index(['time_x', 'type_x', 'id', 'size_x', 'price_x', 'direction_x', 'time_y',

'type_y', 'size_y', 'price_y', 'direction_y'],

dtype='object')

df = message_temp[['id', 'time_x', 'time_y', 'size_y', 'price_x', 'direction_x']]

df.columns = ['id', 'ts', 'te', 'size', 'price', 'direction']

df['duration'] = df.te - df.ts

df.shape

(15099, 7)

Here I defined a function impact to calculate the market impact (reflected on price deviation), such that for each successful execution, we calculate the price change after the same duration of the order.

def impact(idx):

S0, t, duration = df.loc[idx, ['price', 'te', 'duration']]

i = None

for i in range(message_exec[message_exec.time==t].index[0], len(message_exec)):

try:

T = message_exec.loc[i, 'time']

ST = message_exec.loc[i, 'price']

if T - t >= duration: break

except:

pass

if not i: return np.nan

return ST - S0

df['impact'] = [impact(i) for i in df.index]

df_reg = df.dropna()[['size', 'impact']]

df_reg.columns = ['dQ', 'dS']

df_reg.dS = df_reg.dS.abs()

df_reg.T

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | … | 2456 | 2457 | 2458 | 2459 | 2460 | 2461 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| dQ | 1.0 | 10.0 | 9.00 | 40.00 | 18.00 | 100.00 | 18.00 | … | 10.00 | 40.00 | 50.00 | 1.00 | 100.00 | 100.00 |

| dS | 0.2 | 0.2 | 0.03 | 0.19 | 0.07 | 0.09 | 0.21 | … | 0.05 | 0.05 | 0.05 | 0.08 | 0.08 | 0.03 |

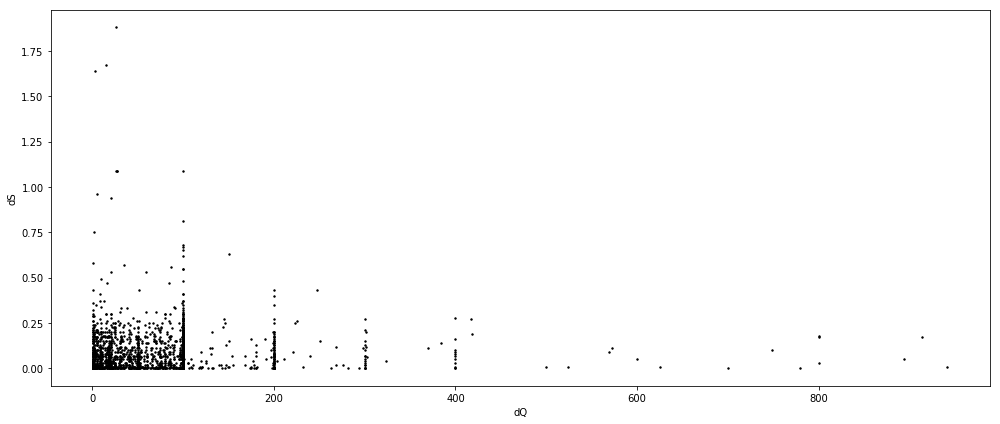

fig = plt.figure(figsize=(14, 6))

ax = fig.add_subplot(111)

ax.scatter(df_reg.dQ, df_reg.dS, color='k', s=2)

ax.set_xlabel('dQ')

ax.set_ylabel('dS')

plt.tight_layout()

plt.show()

res = sm.ols(formula='dS ~ dQ + 0', data=df_reg).fit()

print(res.summary())

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.148

Model: OLS Adj. R-squared: 0.148

Method: Least Squares F-statistic: 427.7

Date: Sat, 12 May 2018 Prob (F-statistic): 1.01e-87

Time: 14:02:16 Log-Likelihood: 1535.7

No. Observations: 2459 AIC: -3069.

Df Residuals: 2458 BIC: -3064.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 0.0005 2.37e-05 20.680 0.000 0.000 0.001

==============================================================================

Omnibus: 2646.045 Durbin-Watson: 1.287

Prob(Omnibus): 0.000 Jarque-Bera (JB): 323199.873

Skew: 5.154 Prob(JB): 0.00

Kurtosis: 58.210 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Apparently there’re several outliers that result in a low $R^2$. Here we remove outliers that are lying outside three standard deviations.

df_reg_no = df_reg[((df_reg.dQ - df_reg.dQ.mean()).abs() < df_reg.dQ.std() * 3) &

((df_reg.dS - df_reg.dS.mean()).abs() < df_reg.dS.std() * 3)]

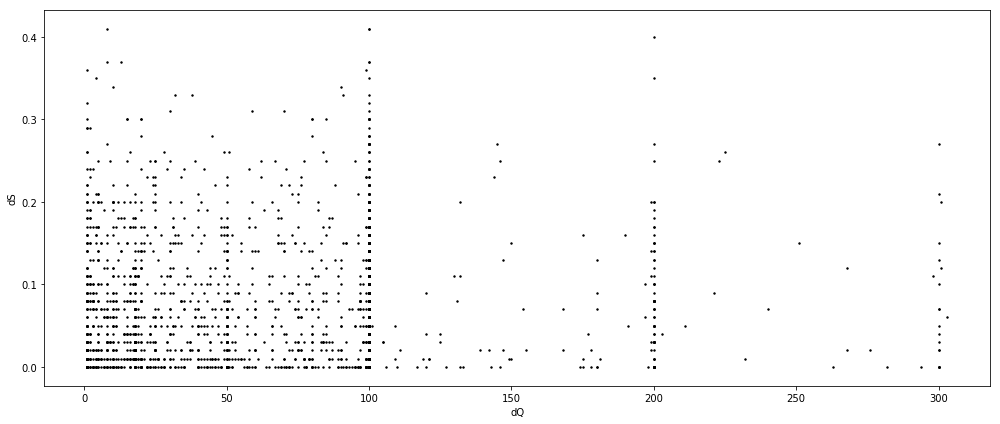

fig = plt.figure(figsize=(14, 6))

ax = fig.add_subplot(111)

ax.scatter(df_reg_no.dQ, df_reg_no.dS, color='k', s=2)

ax.set_xlabel('dQ')

ax.set_ylabel('dS')

plt.tight_layout()

plt.show()

res = sm.ols(formula='dS ~ dQ + 0', data=df_reg_no).fit()

print(res.summary())

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.296

Model: OLS Adj. R-squared: 0.295

Method: Least Squares F-statistic: 1005.

Date: Sat, 12 May 2018 Prob (F-statistic): 1.45e-184

Time: 14:02:20 Log-Likelihood: 2470.2

No. Observations: 2397 AIC: -4938.

Df Residuals: 2396 BIC: -4933.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 0.0006 1.97e-05 31.710 0.000 0.001 0.001

==============================================================================

Omnibus: 356.596 Durbin-Watson: 1.108

Prob(Omnibus): 0.000 Jarque-Bera (JB): 567.767

Skew: 1.012 Prob(JB): 5.14e-124

Kurtosis: 4.259 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

So we conclude $\hat{\eta}_{\text{AAPL}}=0.0006$ for the underlying timespan. However, what about other companies? The coefficients are expected to vary largely, which is though the very worst case we’d like to see.

Comparison

We first define a function estimate to automate what we’ve done above.

def estimate(symbol):

message = pd.read_csv('data/{}_2012-06-21_34200000_57600000_message_1.csv'.format(symbol), header=None)

message.columns = ['time', 'type', 'id', 'size', 'price', 'direction']

message.price /= 10000

message_plce = message[message.type==1]

message_exec = message[message.type==4]

message_temp = pd.merge(message_plce, message_exec, on='id', how='inner')

df = message_temp[['id', 'time_x', 'time_y', 'size_y', 'price_x', 'direction_x']]

df.columns = ['id', 'ts', 'te', 'size', 'price', 'direction']

df['duration'] = df.te - df.ts

def impact(idx):

S0, t, duration = df.loc[idx, ['price', 'te', 'duration']]

i = None

for i in range(message_exec[message_exec.time==t].index[0], len(message_exec)):

try:

T = message_exec.loc[i, 'time']

ST = message_exec.loc[i, 'price']

if T - t >= duration: break

except:

pass

if not i: return np.nan

return ST - S0

df['impact'] = [impact(i) for i in df.index]

df_reg = df.dropna()[['size', 'impact']]

df_reg.columns = ['dQ', 'dS']

df_reg.dS = df_reg.dS.abs()

df_reg_no = df_reg[((df_reg.dQ - df_reg.dQ.mean()).abs() < df_reg.dQ.std() * 3) &

((df_reg.dS - df_reg.dS.mean()).abs() < df_reg.dS.std() * 3)]

res = sm.ols(formula='dS ~ dQ + 0', data=df_reg_no).fit()

print(res.summary())

The estimation for Microsoft Corp. (symbol: MSFT) is as follows.

estimate('MSFT')

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.229

Model: OLS Adj. R-squared: 0.228

Method: Least Squares F-statistic: 550.7

Date: Sat, 12 May 2018 Prob (F-statistic): 7.20e-107

Time: 14:04:51 Log-Likelihood: 5732.8

No. Observations: 1859 AIC: -1.146e+04

Df Residuals: 1858 BIC: -1.146e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 1.859e-05 7.92e-07 23.467 0.000 1.7e-05 2.01e-05

==============================================================================

Omnibus: 201.842 Durbin-Watson: 0.778

Prob(Omnibus): 0.000 Jarque-Bera (JB): 381.770

Skew: 0.703 Prob(JB): 1.26e-83

Kurtosis: 4.719 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The estimation for Amazon.com, Inc. (symbol: AMZN) is as follows.

estimate('AMZN')

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.294

Model: OLS Adj. R-squared: 0.293

Method: Least Squares F-statistic: 328.9

Date: Sat, 12 May 2018 Prob (F-statistic): 1.02e-61

Time: 14:06:56 Log-Likelihood: 809.19

No. Observations: 791 AIC: -1616.

Df Residuals: 790 BIC: -1612.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 0.0007 3.74e-05 18.136 0.000 0.001 0.001

==============================================================================

Omnibus: 141.501 Durbin-Watson: 1.022

Prob(Omnibus): 0.000 Jarque-Bera (JB): 250.801

Skew: 1.083 Prob(JB): 3.46e-55

Kurtosis: 4.709 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The estimation for Alphabet Inc. (symbol: GOOG) is as follows.

estimate('GOOG')

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.419

Model: OLS Adj. R-squared: 0.418

Method: Least Squares F-statistic: 324.2

Date: Sat, 12 May 2018 Prob (F-statistic): 5.96e-55

Time: 14:07:20 Log-Likelihood: 169.55

No. Observations: 450 AIC: -337.1

Df Residuals: 449 BIC: -333.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 0.0017 9.57e-05 18.005 0.000 0.002 0.002

==============================================================================

Omnibus: 48.913 Durbin-Watson: 1.331

Prob(Omnibus): 0.000 Jarque-Bera (JB): 61.896

Skew: 0.864 Prob(JB): 3.63e-14

Kurtosis: 3.563 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The estimation for Intel Corp. (symbol: INTC) is as follows.

estimate('INTC')

OLS Regression Results

==============================================================================

Dep. Variable: dS R-squared: 0.237

Model: OLS Adj. R-squared: 0.237

Method: Least Squares F-statistic: 444.2

Date: Sat, 12 May 2018 Prob (F-statistic): 4.52e-86

Time: 14:08:47 Log-Likelihood: 4480.8

No. Observations: 1429 AIC: -8960.

Df Residuals: 1428 BIC: -8954.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

dQ 2.275e-05 1.08e-06 21.076 0.000 2.06e-05 2.49e-05

==============================================================================

Omnibus: 164.136 Durbin-Watson: 0.716

Prob(Omnibus): 0.000 Jarque-Bera (JB): 284.351

Skew: 0.762 Prob(JB): 1.79e-62

Kurtosis: 4.566 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Conclusion

In sum, the market impact are generally significant but not leading to high $R^2$ values, which suggests the linear assumption might be too strong. Also, it is noteworthy that $\hat{\eta}$ does vary largely between companies (let alone industries or equity types), which means we cannot use one estimation as a benchmark for general production usage.