Spread Trading: XOP and DRIP

2019-04-23

In this strategy we try to do spread trading based on the M-day (adjusted) returns of two highly related ETFs (exchange-traded funds). The intuition is to hedge the one-sided risks of buy-and-holding one specific ETF with (in expectation) increasing returns, by holding an opposite position of another ETF with decreasing returns. Once we have that the two ETFs’ returns are highly correlated, we can trade and make profit by this sort of pair trading.

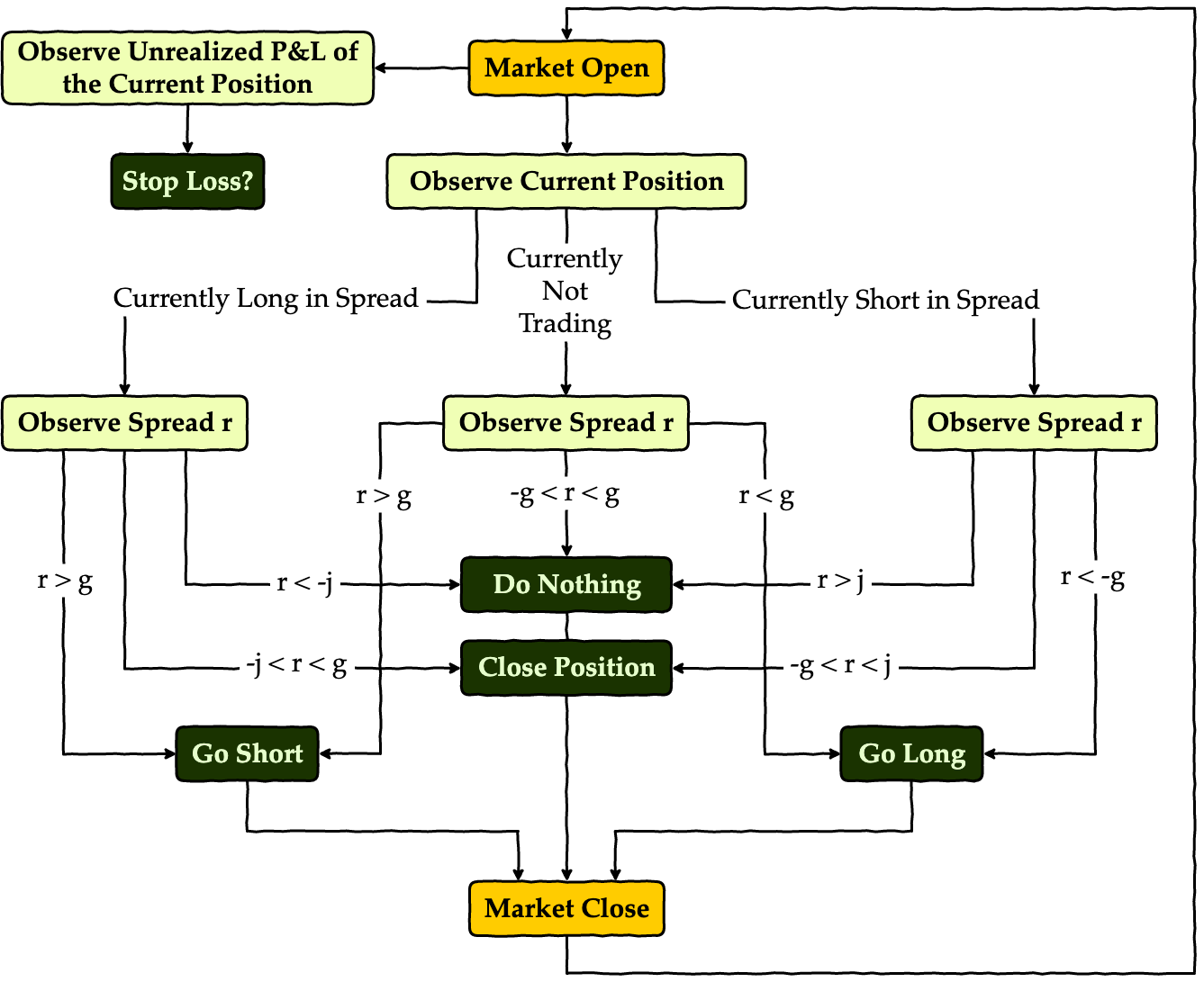

Apart from M, we define trading thresholds g and j, together with stop-loss threshold s. Total capital limit K is assumed to be twice of N, namely the 15-day rolling median volume (of the less liquid ETF). Specifically, we first calculate the array of daily minimums of the two (adjusted) volume series, and then calculate the 15-day rolling median of this series as N. Apart from the capital limit, we also define daily position value (if any) based on N, which is N/100.

Specifically, for each trading day, we have workflow as below.

Apart from this process, we also keep track of our risk exposure with a stop-loss threshold, and try to do trading only within a month’s time, i.e. we start trading only when it’s the start of a new month, and kill any position every time it’s the end of a month.

Dependencies

Import necessary modules and set up corresponding configurations. In this research notebook, we are using the following packages:

- Quandl: source of financial data

- NumPy: mathematical tools & matrix processing

- Pandas: data frame support

- Matplotlib: plotting

- SciPy: statistical analysis

- StatsModels: statistical analysis

import warnings

import quandl

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import norm, t

from statsmodels.tsa.stattools import adfuller

pd.set_option('display.max_rows', 30)

plt.style.use('bmh')

plt.rcParams['font.family'] = 'serif'

plt.rcParams['font.size'] = 15

warnings.filterwarnings('ignore')

quandl.ApiConfig.api_key = QUANDL_API_KEY

Preparatory Analysis

In this part, we will try to analyze the economic and statistical features in the data. Here the two ETFs we’re using are XOP and DRIP. Data is retrieved from Quandl from 2015-12-02 to 2018-12-31. We’ll use only data from 2015-12-02 to 2016-12-01 for this section, as we don’t want to include future information during the backtest. Also, while it’s always better to have longer historical data for analysis, due to limited length of ETF data on Quandl (specifically for these two ETFs) we’re unfortunately restrained to this short timespan.

Definition of XOP

The SPDR S&P Oil & Gas Exploration & Production ETF (XOP) seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of the S&P Oil & Gas Exploration & Production Select Industry Index. See here for more detailed description.

Definition of DRIP

The Direxion Daily S&P Oil & Gas Exp. & Prod. Bull and Bear 3X Shares (DRIP) seek daily investment results, before fees and expenses, of 300% of the inverse, of the performance of the S&P Oil & Gas Exploration & Production Select Industry Index. See here for more detailed description.

Relationship of XOP and DRIP

By definition of the two ETFs, we expect DRIP to track -300% the daily return of XOP. This means the spread we should be tracking is, instead of the return difference between the two, the difference of -300% of M-day returns of XOP and the M-day returns of DRIP. Also, we are supposed to hold, if any, positions of these two ETFs in a ratio of XOP:DRIP = -3, no matter we’re long or short in the spread.

A peek into the data (assume M is 5.):

DRIP: price of DRIPXOP: price of XOPrDRIP: 5-day return of DRIPrXOP: 5-day return of XOPrXOPn3: -300% of 5-day return of XOPspread: spread ofrXOPn3fromrDRIP(spread = rDRIP - rXOPn3)

The first few entries of our data reads:

# exploratory settings

symbols = ('DRIP', 'XOP')

dates = ('2015-12-02', '2016-12-01')

M = 5

# retrieve data

df_X = quandl.get('EOD/' + symbols[0], start_date=dates[0], end_date=dates[1])

df_Y = quandl.get('EOD/' + symbols[1], start_date=dates[0], end_date=dates[1])

X = df_X.Adj_Close

Y = df_Y.Adj_Close

# calculate M-day returns

rX = (X.diff(M) / X.shift(M)).dropna()

rY = (Y.diff(M) / Y.shift(M)).dropna()

rY3 = rY * -3

spread = rX - rY3

# concat all variables

df = pd.concat([X, Y, rX, rY, rY3, spread], axis=1).dropna()

del X, Y, rX, rY, rY3, spread, df_X, df_Y

df.columns = [symbols[0], symbols[1],

'r' + symbols[0], 'r' + symbols[1],

'r' + symbols[1] + 'n3', 'spread']

df.head(10)

| Date | DRIP | XOP | rDRIP | rXOP | rXOPn3 | spread |

|---|---|---|---|---|---|---|

| 2015-12-09 | 93.228406 | 31.481858 | 0.300551 | -0.091874 | 0.275621 | 0.024930 |

| 2015-12-10 | 87.783600 | 32.033661 | 0.175401 | -0.063402 | 0.190207 | -0.014806 |

| 2015-12-11 | 100.660997 | 30.465377 | 0.247456 | -0.084908 | 0.254725 | -0.007269 |

| 2015-12-14 | 107.982471 | 29.719958 | 0.113006 | -0.041524 | 0.124571 | -0.011565 |

| 2015-12-15 | 101.685757 | 30.310485 | 0.065597 | -0.028545 | 0.085635 | -0.020037 |

| 2015-12-16 | 108.538063 | 29.632831 | 0.164217 | -0.058733 | 0.176199 | -0.011983 |

| 2015-12-17 | 118.711577 | 28.616350 | 0.352321 | -0.106679 | 0.320036 | 0.032284 |

| 2015-12-18 | 125.551661 | 28.154731 | 0.247272 | -0.075845 | 0.227535 | 0.019737 |

| 2015-12-21 | 130.267899 | 27.862871 | 0.206380 | -0.062486 | 0.187459 | 0.018921 |

| 2015-12-22 | 125.008291 | 28.203374 | 0.229359 | -0.069518 | 0.208553 | 0.020806 |

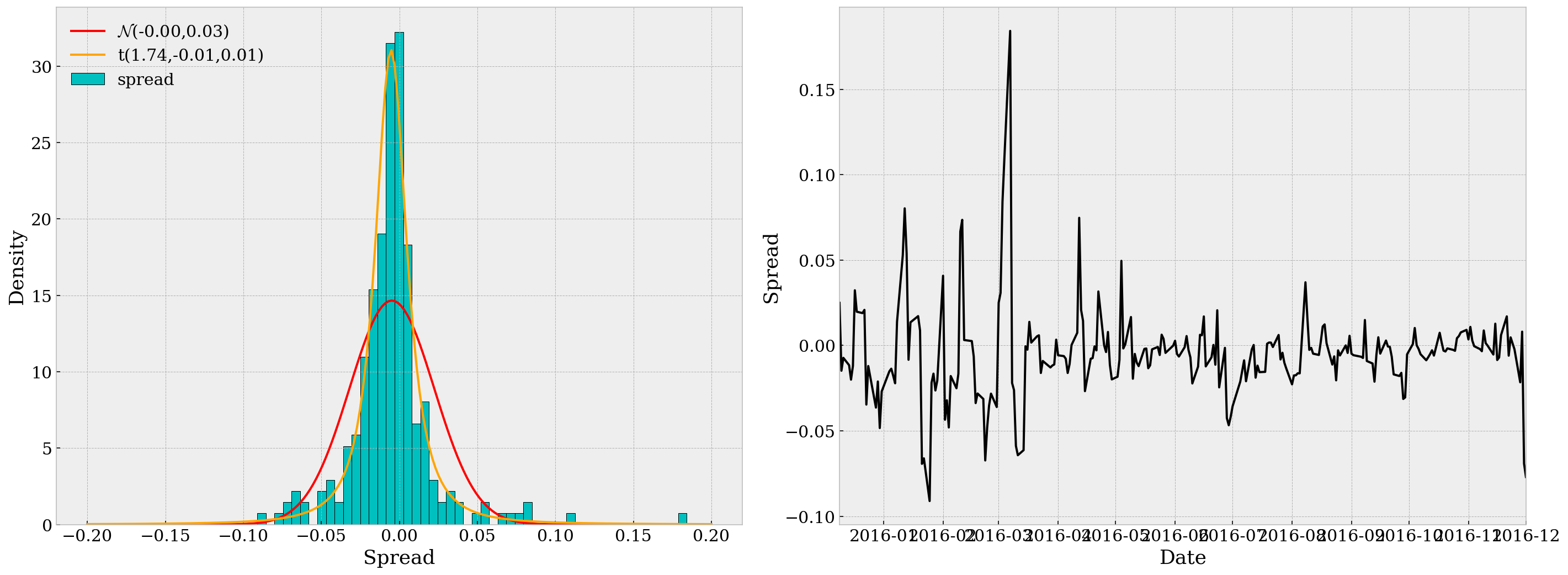

Also we may plot the histogram of the spread. Here we plot it against the fitted normal and t distributions. Apparently the t distribution matches our spread data better, which coincides with our expectation as financial data is commonly seen with fat tails. Also, we may notice that the spread is well centered around zero, which reassures us that we can assume symmetrical thresholds for trading.

fig = plt.figure(figsize=(20, 7.5))

ax = fig.add_subplot(121)

ax.hist(df.spread, bins=50, edgecolor='k', facecolor='c', density=True)

x_grid = np.linspace(-.2, .2, 200)

# fit to normal

params = norm.fit(df.spread)

pdf_fitted = norm.pdf(x_grid, *params)

plt.plot(x_grid, pdf_fitted, color='r',

label='$\mathcal{N}$' + '({:.2f},{:.2f})'.format(*params))

# fit to t

params = t.fit(df.spread)

pdf_fitted = t.pdf(x_grid, *params)

plt.plot(x_grid, pdf_fitted, color='orange',

label='t({:.2f},{:.2f},{:.2f})'.format(*params))

ax.set_xlabel('Spread')

ax.set_ylabel('Density')

ax.legend(frameon=False, loc='upper left')

ax = fig.add_subplot(122)

df.spread.plot(ax=ax, color='k')

plt.xticks(rotation=0, ha='center')

ax.set_xlabel('Date')

ax.set_ylabel('Spread')

plt.tight_layout()

plt.show()

In the second subplot, we can see that the spread series is quite “stationary” over time, but we’d better not stop just observing by eye. (Also it’s a bit heteroskedastic, but we’re not focusing on that in this research.)

Statistical Tests

Below are some statistical tests we need to run through before actual pair traing. For detailed reasoning please refer to this post.

- Test for Unit Root: Here we use the Augmented Dickey-Fuller test. The p-value is 6.35e-14 $\ll$ 0.05, so we may safely reject the null.

result = adfuller(df.spread)

print('ADF Statistic: {}\np-value: {}\nCritical Values:'.format(*result[:2]))

for key, value in result[4].items():

print('\t{}: {:.3f}'.format(key, value))

ADF Statistic: -8.614239430241229

p-value: 6.353844261802846e-14

Critical Values:

1%: -3.458

5%: -2.874

10%: -2.573

- Test for Strong Stationarity: Here we opt for the Hurst Exponent. By definition, Hurst value H < 0.5 indicates the time series is mean-reverting, and our H value for the spread is -0.0390, so assumption is confirmed.

def hurst(ts):

lags = range(2, 100)

tau = [np.sqrt(np.std(np.subtract(ts[lag:], ts[:-lag]))) for lag in lags]

poly = np.polyfit(np.log(lags), np.log(tau), 1)

return poly[0]*2.0

np.random.seed(123)

gbm = np.log(np.cumsum(np.random.randn(100000))+1000)

mr = np.log(np.random.randn(100000)+1000)

tr = np.log(np.cumsum(np.random.randn(100000)+1)+1000)

print('H: {:.4f}'.format(hurst(df.spread)))

H: -0.0390

Based on the previous two test results we conclude our spread is mean-reverting and the strategy is reasonable.

Backtest Engine

In this part we design a simple backtest engine that takes ETF symbols, backtest timespan and the theoretical return ratio. It then provides an interface to run backtest against different parameters. I’ve encapsulated private methods/variables in the class BacktestEngine and there are only three attributes available:

BacktestEngine.symbols: tuple of ETF symbolsBacktestEngine.run: run backtest (returns Sortino ratio, Sharpe ratio, maximum drawdown and YoY return)BacktestEngine.df: stores the data from backtest (trade log)

The basic usage of this engine would be

be = BacktestEngine('DRIP', 'XOP', '2016-12-02', '2018-12-31', ratio=-3)

be.run(M=5, g=0.010, j=0.005, s=0.010, verbose=True) # plot the backtest results

and if you want to check the tradelog during the timespan, call be.df. Note in this data frame, we denote the two ETFs by X and Y, and instead of the original M-day return of Y, we denote rY as ratio times the original M-day returns. The positions of X and Y are also reported in be.df together with daily and cumulative returns (in percentages of K).

An example of this be.df would be

| Date | X | Y | rX | rY | spread | N | pX | pY | daily_rtn | cum_rtn |

|---|---|---|---|---|---|---|---|---|---|---|

| 2016-12-22 | 12.267480 | 41.323160 | -0.019732 | -0.017567 | -0.002165 | 1.549400e+07 | 0 | 0 | 0.0 | 0.0 |

| 2016-12-23 | 12.208217 | 41.450761 | -0.017488 | -0.015711 | -0.001778 | 1.210184e+07 | 0 | 0 | 0.0 | 0.0 |

| 2016-12-27 | 12.000796 | 41.666701 | -0.018578 | -0.016343 | -0.002235 | 1.064284e+07 | 0 | 0 | 0.0 | 0.0 |

| 2016-12-28 | 12.445270 | 41.166112 | 0.003185 | 0.004286 | -0.001101 | 9.867562e+06 | 0 | 0 | 0.0 | 0.0 |

| 2016-12-29 | 12.692200 | 40.901094 | 0.017419 | 0.017180 | 0.000239 | 9.607867e+06 | 0 | 0 | 0.0 | 0.0 |

class BacktestEngine:

def __init__(self, X_symbol, Y_symbol, start_date, end_date, ratio=1):

'''

PARAMETER:

X_symbol: string

Y_symbol: string

start_date: string or datetime object

end_date: string or datetime object

RETURN: None

'''

self.symbols = (X_symbol, Y_symbol)

self.__dates = (start_date, end_date)

self.__stop_loss_dates = []

self.__ratio = ratio

# load data

df_X = quandl.get('EOD/' + self.symbols[0],

start_date=self.__dates[0],

end_date=self.__dates[1])

df_Y = quandl.get('EOD/' + self.symbols[1],

start_date=self.__dates[0],

end_date=self.__dates[1])

self.__data = [df_X, df_Y]

self.__trading = False

def __process_data(self): # prepare data to feed model

'''

PARAMETER: None

RETURN: None

'''

df_X, df_Y = self.__data

# generate price and volume series

N_X = df_X.Adj_Volume * df_X.Adj_Close

N_Y = df_Y.Adj_Volume * df_Y.Adj_Close

N = pd.concat([N_X, N_Y], axis=1).min(axis=1).rolling(15).median()

self.__K = N.max() * 2

X = df_X.Adj_Close

Y = df_Y.Adj_Close

# calculate M-day returns

M = self.__M

rX = (X.diff(M) / X.shift(M)).dropna()

rY = (Y.diff(M) / Y.shift(M)).dropna() * self.__ratio

spread = rX - rY

# concat all variables

df = pd.concat([X, Y, rX, rY, spread, N], axis=1).dropna()

del X, Y, rX, rY, spread, N

df.columns = ['X', 'Y', 'rX', 'rY', 'spread', 'N']

self.df = df

def __update_params(self, M, g, j, s): # update parameters of the model

'''

PARAMETER:

M: integer

g: float

j: float

s: float

RETURN: None

'''

assert isinstance(M, (int, np.integer)) and (M > 0), \

'parameter M should be a positive integer'

assert -g < j < g, 'parameter j and g should follow -g < j < g'

assert 0 < s, 'parameter s should be positive'

self.__M = M

self.__g = g

self.__j = j

self.__s = s

self.__process_data()

@staticmethod

def __posval(position, price1, price2, gross=False): # calculate value

'''

PARAMETER:

position: float

price1: float

price2: float

grodd: boolean (default: False)

RETURN: float

'''

if gross:

return abs(position[0]) * price1 + abs(position[1]) * price2

else:

return position[0] * price1 + position[1] * price2

def __pos(self, value, X, Y, longX=True): # calculate positions

'''

PARAMETER:

value: float

X: float

Y: float

longX: boolean (default: True)

RETURN: (float, float)

'''

pX = round(value / X) * abs(self.__ratio)

pY = round(value / Y) * (1 if self.__ratio > 0 else -1)

return (pX, -pY) if longX else (-pX, pY)

@staticmethod

def __sharpe_ratio(daily_rtn): # calculate sharpe ratio

'''

PARAMETER:

daily_rtn: pd.Series of float

RETURN: float

'''

return daily_rtn.mean() / daily_rtn.std()

@staticmethod

def __sortino_ratio(daily_rtn): # calculate sortino ratio

'''

PARAMETER:

daily_rtn: pd.Series of float

RETURN: float

'''

daily_rtn = daily_rtn.copy()

mean_rtn = daily_rtn.mean()

daily_rtn.loc[daily_rtn > 0] = 0

downside_risk = daily_rtn.std()

return mean_rtn / downside_risk

@staticmethod

def __maximum_drawdown(value): # maximum drawdown

'''

PARAMETER:

value: pd.Series of float

RETURN: (float, datetime, datetime)

'''

end = (value.cummax() / value).idxmax()

start = (value.loc[:end]).idxmax()

mdd = 1 - value[end] / value[start]

return mdd, start, end

def run(self, M, g, j, s, verbose=True): # run backtest using parameters

'''

PARAMETER:

M: integer

g: float

j: float

s: float

verbose: boolean (default: True)

RETURN: None

'''

self.__update_params(M, g, j, s)

pX = []

pY = [] # positions

rtn = []

curr_position = (0, 0)

curr_rtn = 0

prev_day = 0

prev_cost = 0

prev_gross_cost = 0

spread = 0

for date in self.df.index:

if date.day < prev_day: # check start of new month

daily_rtn = curr_rtn

curr_position = (0, 0)

prev_cost = 0

prev_gross_cost = 0

self.__trading = True

elif self.__trading: # trading (never stop-lossed this month)

if curr_rtn < -self.__s * prev_gross_cost: # stop loss

self.__stop_loss_dates.append(date)

daily_rtn = curr_rtn

curr_position = (0, 0)

prev_cost = prev_gross_cost = 0

self.__trading = False

else:

if curr_position[0] > 1: # currently long in X

daily_rtn = curr_rtn

if spread > self.__g: # direactly from long to short

curr_position = self.__pos(N / 100, X, Y, False)

prev_cost = self.__posval(curr_position, X, Y)

prev_gross_cost = self.__posval(curr_position, X, Y, True)

elif spread > -self.__j: # close position

curr_position = (0, 0)

prev_cost = prev_gross_cost = 0

elif curr_position[0] < -1: # currently short in X

daily_rtn = curr_rtn

if spread < -self.__g: # directly from short to long

curr_position = self.__pos(N / 100, X, Y, True)

prev_cost = self.__posval(curr_position, X, Y)

prev_gross_cost = self.__posval(curr_position, X, Y, True)

elif spread < self.__j: # close position

curr_position = (0, 0)

prev_cost = prev_gross_cost = 0

else: # currently having no position

daily_rtn = 0

if spread > self.__g: # open short position

curr_position = self.__pos(N / 100, X, Y, False)

prev_cost = self.__posval(curr_position, X, Y)

prev_gross_cost = self.__posval(curr_position, X, Y, True)

elif spread < -self.__g: # open long position

curr_position = self.__pos(N / 100, X, Y, True)

prev_cost = self.__posval(curr_position, X, Y)

prev_gross_cost = self.__posval(curr_position, X, Y, True)

else: # ceased until next month

daily_rtn = 0

spread, X, Y, N = self.df[['spread', 'X', 'Y', 'N']].loc[date]

curr_rtn = self.__posval(curr_position, X, Y) - prev_cost

pX.append(curr_position[0])

pY.append(curr_position[1])

rtn.append(daily_rtn)

prev_day = date.day

self.df['pX'] = pX

self.df['pY'] = pY

self.df['daily_rtn'] = rtn

self.df.daily_rtn /= self.__K # rtn is stored in %

self.df['cum_rtn'] = self.df.daily_rtn.cumsum()

sortino = self.__sortino_ratio(self.df.daily_rtn)

sharpe = self.__sharpe_ratio(self.df.daily_rtn)

mdd = self.__maximum_drawdown(self.df.cum_rtn + self.__K)[0]

yoy_rtn = (1 + self.df.cum_rtn[-1])**(250 / self.df.shape[0]) - 1

if verbose: self.__plot()

return sortino, sharpe, mdd, yoy_rtn

def __plot(self): # plot backtest results

'''

PARAMETER: None

RETURN: None

'''

fig = plt.figure(figsize=(20, 15))

ax1 = fig.add_subplot(221)

self.df.rX.plot(ax=ax1, label='X', alpha=.5, color='darkgreen')

self.df.rY.plot(ax=ax1, label='Y', color='pink')

ax1.set_ylabel('Returns')

self.df.spread.plot(ax=ax1, label='spread', color='k')

plt.xticks(rotation=0, ha='center')

plt.legend(frameon=False, loc='upper right')

ax2 = fig.add_subplot(222)

self.df.spread.plot(ax=ax2, label='spread', color='k')

ax2.plot((min(self.df.index), max(self.df.index)),

(self.__g, self.__g), 'c--', label='$\pm$g')

ax2.plot((min(self.df.index), max(self.df.index)),

(self.__j, self.__j), 'r--', label='$\pm$j')

ax2.plot((min(self.df.index), max(self.df.index)),

(-self.__g, -self.__g), 'c--')

ax2.plot((min(self.df.index), max(self.df.index)),

(-self.__j, -self.__j), 'r--')

ax2.set_ylabel('Spread')

plt.xticks(rotation=0, ha='center')

plt.legend(frameon=False)

mdd, sd, ed = self.__maximum_drawdown(self.df.cum_rtn + self.__K)

ax3 = fig.add_subplot(223)

self.df.N.plot(ax=ax3, label='N', color='k')

ax3.set_ylabel('Total Dollar Volumes')

plt.legend(frameon=False, loc='upper left')

plt.xticks(rotation=0, ha='center')

ax3_ = ax3.twinx()

self.df.pX.abs().plot(ax=ax3_, label='position', alpha=.5, color='r')

ax3_.ticklabel_format(axis='y', style='sci', scilimits=(5, 5))

ax3_.axvspan(xmin=sd, xmax=ed, ymin=0, ymax=1, color='grey', alpha=.5)

ax3_.set_ylim(ymin=0)

ax3_.set_ylabel('Daily Position (Long)')

ax3.grid(False)

plt.legend(frameon=False, loc='upper right')

ax4 = fig.add_subplot(224)

ax4.axvspan(xmin=sd, xmax=ed, ymin=0, ymax=1, color='grey', alpha=.5)

(self.df.daily_rtn * 100).plot(ax=ax4, label='Daily Return (%)', color='c')

(self.df.cum_rtn * 100).plot(ax=ax4, label='Cum. Return (%)', color='r')

ax4.scatter(self.__stop_loss_dates,

self.df.cum_rtn.loc[self.__stop_loss_dates] * 100,

marker='x', color='k', label='', zorder=10)

ax4.set_ylabel('Return (%)')

plt.xticks(rotation=0, ha='center')

plt.legend(frameon=False)

plt.tight_layout()

plt.show()

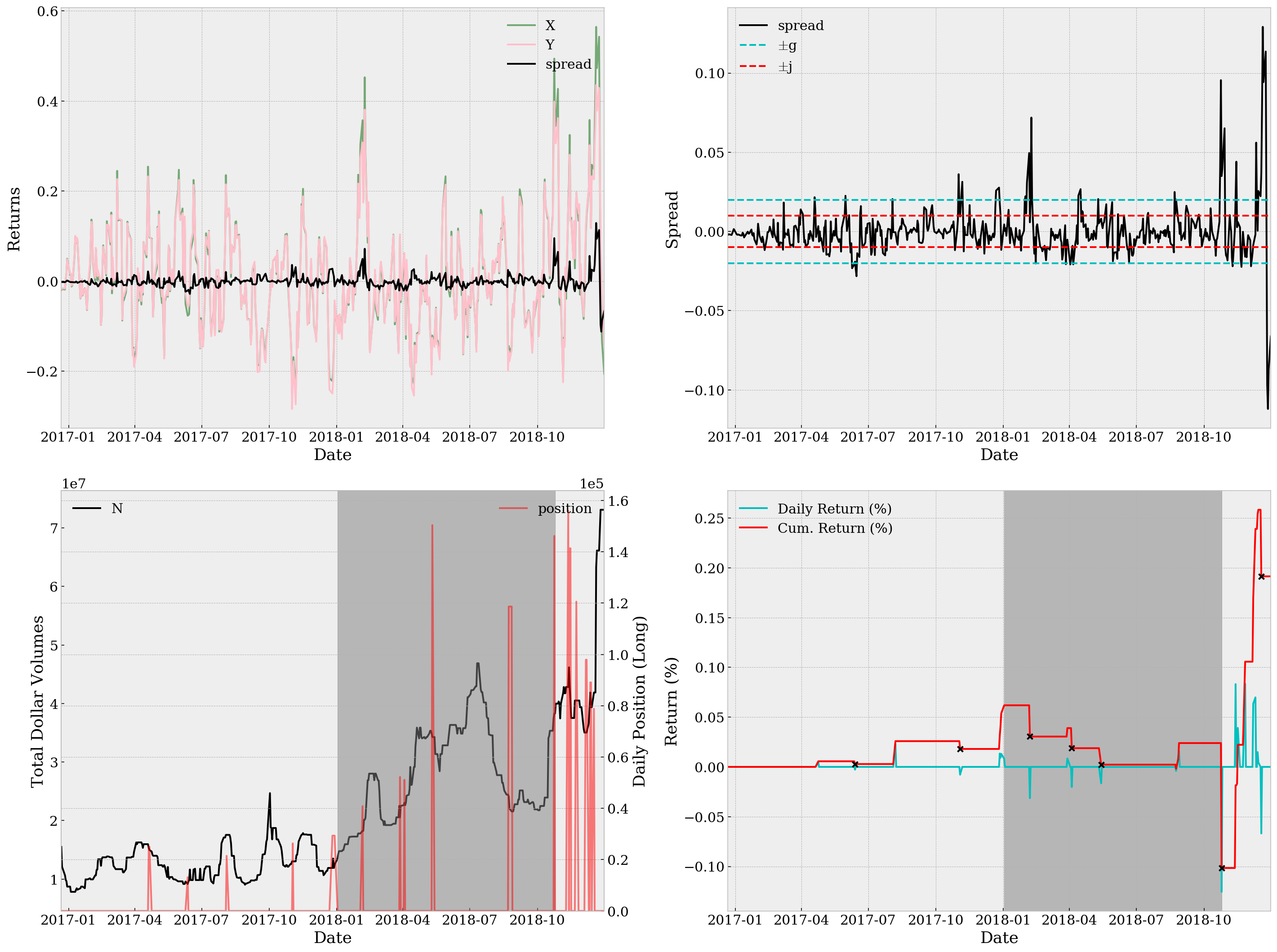

Here for illustration, we make a test run with parameters M=5, g=0.010, j=0.005 and s=0.01. The timespan, as required throughout the analysis, is set from 2016-12-02 to 2018-12-31 inclusive. The special meta parameter ratio is set to -3.

be = BacktestEngine('DRIP', 'XOP', start_date='2016-12-02', end_date='2018-12-31', ratio=-3)

st, sr, md, rt = be.run(M=5, g=0.02, j=0.01, s=0.01, verbose=True)

print('Sortino Ratio={:.4f}, Sharpe Ratio={:.4f}, Maximum Drawdown={:.4g}, YoY Return={:.2%}'

.format(st, sr, md ,rt))

Sortino Ratio=0.0574, Sharpe Ratio=0.0387, Maximum Drawdown=1.118e-11, YoY Return=0.09%

With only a Sortino ratio of 0.0574, a Sharpe ratio of 0.0387 and YoY return of 0.09%, it’s definitely not a good strategy. Not to mention the unsatisfactory return plots. The top right subplot together with the bottom left one suggests that we might be using too wide thresholds. In case of detailed analysis, we can also take a look at be.df and specifically the trading days when we have non-zero positions, which turns out rather few (and supports our worry about wideness of thresholds):

be.df.loc[be.df.pX != 0]

| Date | X | Y | rX | rY | spread | N | pX | pY | daily_rtn | cum_rtn |

|---|---|---|---|---|---|---|---|---|---|---|

| 2017-04-20 | 19.072870 | 34.413981 | 0.191975 | 0.178984 | 0.012991 | 1.533244e+07 | -25014 | -4643 | 0.000000 | 0.000000 |

| 2017-04-21 | 18.845694 | 34.532005 | 0.097182 | 0.100743 | -0.003561 | 1.496846e+07 | -25014 | -4643 | 0.000011 | 0.000011 |

| 2017-06-12 | 21.522415 | 32.279704 | -0.076695 | -0.055866 | -0.020829 | 9.166219e+06 | 13122 | 2984 | 0.000000 | 0.000056 |

| 2017-08-04 | 22.747188 | 30.827585 | 0.142928 | 0.143423 | -0.000495 | 1.754893e+07 | -21483 | -5827 | 0.000000 | 0.000029 |

| 2017-11-02 | 15.319535 | 34.463445 | -0.210285 | -0.227637 | 0.017352 | 1.302198e+07 | -26349 | -3734 | 0.000000 | 0.000259 |

| 2017-12-26 | 11.398287 | 37.260895 | -0.221848 | -0.249496 | 0.027649 | 1.189655e+07 | -29352 | -3264 | 0.000000 | 0.000180 |

| 2017-12-27 | 11.645217 | 36.963916 | -0.200136 | -0.218041 | 0.017905 | 1.351392e+07 | -29352 | -3264 | 0.000135 | 0.000315 |

| 2017-12-28 | 11.418041 | 37.241096 | -0.152493 | -0.163117 | 0.010624 | 1.189655e+07 | -29352 | -3264 | 0.000092 | 0.000406 |

| 2017-12-29 | 11.714357 | 36.805528 | -0.054226 | -0.042553 | -0.011673 | 1.246303e+07 | -29352 | -3264 | 0.000131 | 0.000537 |

| 2018-02-05 | 14.331815 | 34.023830 | 0.357343 | 0.307833 | 0.049510 | 1.823786e+07 | -40842 | -5061 | 0.000000 | 0.000619 |

| 2018-03-28 | 13.193795 | 33.978894 | 0.097942 | 0.103973 | -0.006031 | 2.054748e+07 | 52227 | 6579 | 0.000000 | 0.000305 |

| 2018-04-03 | 12.630042 | 34.326023 | 0.045008 | 0.062801 | -0.017792 | 2.304128e+07 | 51093 | 6703 | 0.000000 | 0.000390 |

| 2018-05-11 | 7.140870 | 40.931377 | -0.120585 | -0.125726 | 0.005141 | 3.427444e+07 | -150390 | -8464 | 0.000000 | 0.000188 |

| 2018-08-23 | 6.237512 | 41.241724 | -0.144022 | -0.155054 | 0.011033 | 2.413513e+07 | -118650 | -5898 | 0.000000 | 0.000023 |

| 2018-08-24 | 6.039495 | 41.778234 | -0.157459 | -0.177582 | 0.020123 | 2.205453e+07 | -118650 | -5898 | -0.000041 | -0.000018 |

| 2018-08-27 | 5.960289 | 41.877588 | -0.146099 | -0.152580 | 0.006481 | 2.155575e+07 | -118650 | -5898 | 0.000098 | 0.000081 |

| 2018-10-24 | 9.096368 | 35.500295 | 0.494290 | 0.398785 | 0.095505 | 3.827526e+07 | -146172 | -9913 | 0.000000 | 0.000239 |

| 2018-11-12 | 9.106299 | 34.953065 | 0.168153 | 0.166935 | 0.001217 | 4.281623e+07 | 156027 | 11825 | 0.000000 | -0.001016 |

| 2018-11-14 | 9.801436 | 34.107346 | 0.324832 | 0.280804 | 0.044028 | 4.281623e+07 | -141351 | -13473 | 0.000000 | -0.000185 |

| 2018-11-15 | 9.364493 | 34.614778 | 0.136145 | 0.133480 | 0.002665 | 4.050823e+07 | -141351 | -13473 | 0.000016 | -0.000169 |

| 2018-11-23 | 11.211572 | 32.336311 | 0.197243 | 0.197471 | -0.000228 | 4.050823e+07 | 120567 | 12081 | 0.000000 | 0.000222 |

| 2018-12-06 | 11.797473 | 31.520441 | 0.111319 | 0.125227 | -0.013908 | 3.503895e+07 | 97920 | 10763 | 0.000000 | 0.001057 |

| 2018-12-07 | 11.906709 | 31.381147 | 0.147368 | 0.155996 | -0.008628 | 3.503895e+07 | 97920 | 10763 | 0.000635 | 0.001692 |

| 2018-12-12 | 12.989137 | 30.475730 | 0.209991 | 0.191626 | 0.018365 | 4.187946e+07 | -89073 | -12988 | 0.000000 | 0.002391 |

| 2018-12-13 | 13.187748 | 30.286687 | 0.117845 | 0.117424 | 0.000421 | 3.936253e+07 | -89073 | -12988 | 0.000148 | 0.002539 |

| 2018-12-17 | 16.375449 | 28.077868 | 0.248297 | 0.226081 | 0.022215 | 4.187946e+07 | -78804 | -13600 | 0.000000 | 0.002583 |

Parameter Tuning

As mentioned above, in this section we try to fit the best set of parameters from 2015-12-02 to 2016-12-01, i.e. the training set. As the focus of this report is not about efficient optimization, we opt for a simple grid search here. The parameter grids are defined as

M_grid: 5, 10, 15, 20 (4 in total)g_grid: 0.001, 0.003, …, 0.011 (6 in total)j_grid: -0.010, -0.008, …, 0.010 (11 in total)s_grid: 1e-3, 5e-3, 1e-2, 5e-2, 1e-1 (5 in total)

So no more than 1320 simulations are run. Note here parameter combinations where -g < j < g does not hold are neglected. Below are a selection of outstanding parameter sets during simulation.

from time import time

from itertools import product

def record():

# record function with closure designed

# to keep track of the best parameters

record.best = []

def f(*args):

record.best.append((*args,))

return f

mst, msr, mmd, mrt = 0, 0, 1, 0

M_grid = np.arange(5, 25, 5)

g_grid = np.arange(0.001, 0.012, 0.002)

j_grid = np.arange(-0.010, 0.011, 0.002)

s_grid = [1e-3, 5e-3, 0.01, 0.05, 0.10]

nsim = len(M_grid) * len(g_grid) * len(j_grid) * len(s_grid)

report_params = record()

be = BacktestEngine('DRIP', 'XOP', start_date='2015-12-02', end_date='2016-12-01', ratio=-3)

start_time = time()

for i, params in enumerate(product(M_grid, g_grid, j_grid, s_grid)):

try:

st, sr, md, rt = be.run(*params, verbose=False)

if np.isnan(sr) or sr < 0 or st < 0: continue

report = False

if st > mst: mst, report = st, True

if sr > msr: msr, report = sr, True

if md < mmd: mmd, report = md, True

if rt > mrt: mrt, report = rt, True

prog = (i + 1) / nsim

current_time = time()

elapse = current_time - start_time

eta = elapse / prog * (1 - prog)

print('Running {} simulations... {:.2%} finished, ETA={:.0f}s'

.format(nsim, prog, eta) + ' ' * 10, end='\r')

if report: report_params(*params, st, sr, md, rt)

except AssertionError: # (-g < j < g) does not hold

continue

st_list, sr_list, md_list, rt_list = list(zip(*record.best))[-4:]

record.best = [entries for _, entries in sorted(zip(st_list, record.best))][-5:]

record.best = [entries for _, entries in sorted(zip(sr_list, record.best))][-5:]

record.best = [entries for _, entries in sorted(zip(rt_list, record.best))][-5:]

record.best = [entries for _, entries in sorted(zip(md_list, record.best))][:5]

for i, entries in enumerate(record.best):

print('(Record {:2}) M={:>2}, g={:.3f}, j={:6.3f}, s={:.5f},\t'

'st={:.4f} sr={:.4f}, md={:9.4g}, rt={:6.2%}'

.format(i, *entries))

(Record 0) M=15, g=0.007, j=-0.004, s=0.05000, st=1.4542 sr=0.3393, md=1.934e-10, rt= 8.99%

(Record 1) M=15, g=0.011, j=-0.010, s=0.05000, st=1.4591 sr=0.3430, md=1.673e-10, rt= 9.17%

(Record 2) M=20, g=0.007, j=-0.006, s=0.05000, st=1.5146 sr=0.3540, md=2.076e-10, rt= 9.47%

(Record 3) M=20, g=0.007, j= 0.006, s=0.05000, st=1.6001 sr=0.3534, md= 1.7e-10, rt= 9.33%

(Record 4) M=15, g=0.011, j=-0.004, s=0.05000, st=1.4680 sr=0.3452, md=1.673e-10, rt= 9.15%

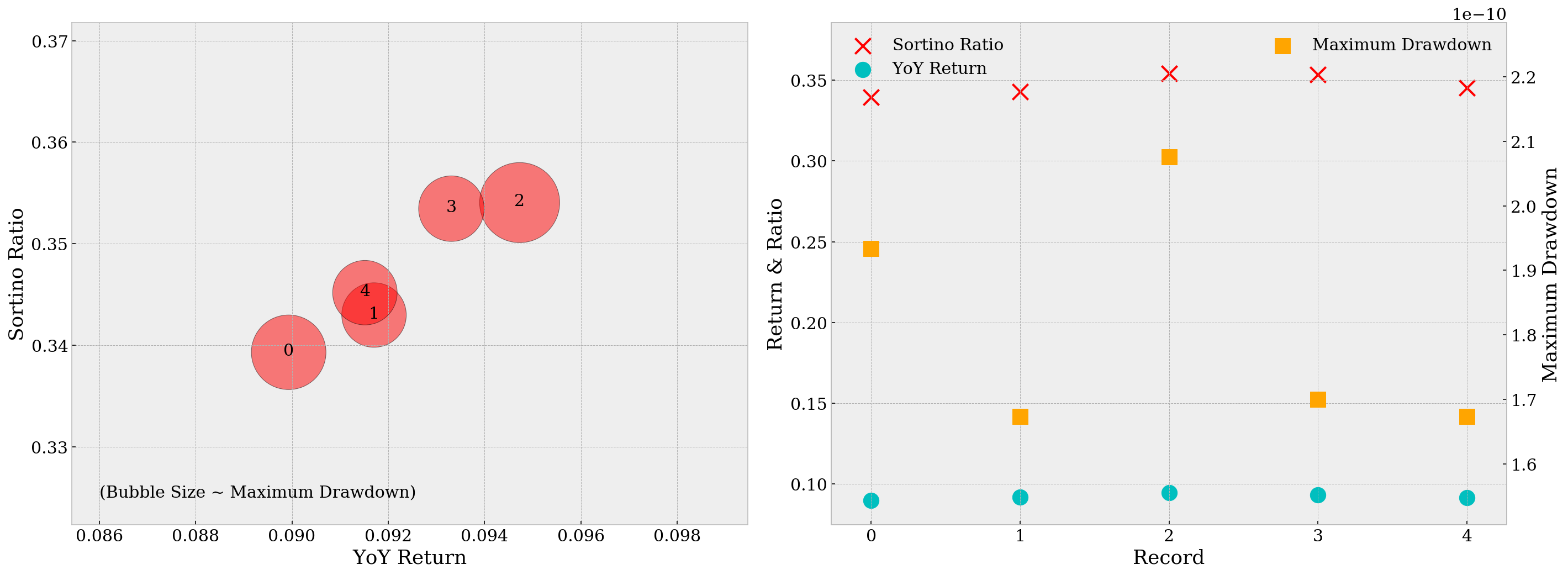

From the two plots below, we can tell that Record 3, or the parameter set M=20, g=0.007, j=0.006, s=0.05000, is a good choice as it has both large Sortino ratio/YoY return and a relatively small maximum drawdown. Record 2, or M=20, g=0.007, j=-0.006, s=0.05000 is also playing well among all outstanding parameter sets, with slightly better Sortino ratio and YoY returns but larger maximum drawdown. We’ll test on both sets.

rec = np.arange(len(record.best))

st_list, st_list, md_list, rt_list = list(zip(*record.best))[-4:]

fig = plt.figure(figsize=(20, 7.5))

ax = fig.add_subplot(121)

ax.set_xlim(min(rt_list) * 0.95, max(rt_list) * 1.05)

ax.set_ylim(min(st_list) * 0.95, max(st_list) * 1.05)

st_offset = (max(st_list) - min(st_list)) * 0.02

ax.scatter(rt_list, st_list, s=[(md / np.mean(md_list))**2 * 4e3 for md in md_list],

color='r', edgecolor='k', alpha=.5)

ax.text(.086, .325, '(Bubble Size ~ Maximum Drawdown)')

for rt, st, i in zip(rt_list, st_list, range(len(record.best))):

ax.text(x=rt, y=st - st_offset, s=str(i), ha='center')

ax.set_xlabel('YoY Return')

ax.set_ylabel('Sortino Ratio')

ax = fig.add_subplot(122)

ax.scatter(rec, st_list, color='r', marker='x', s=200, label='Sortino Ratio')

ax.scatter(rec, rt_list, color='c', marker='o', s=200, label='YoY Return')

ax.set_xlabel('Record')

ax.set_ylabel('Return & Ratio')

ax.legend(frameon=False, loc='upper left')

ax = ax.twinx()

ax.grid(False)

ax.scatter(rec, md_list, color='orange', marker='s', s=200, label='Maximum Drawdown')

ax.set_ylim(min(md_list) * 0.9, max(md_list) * 1.1)

ax.xaxis.set_ticks(rec)

ax.set_ylabel('Maximum Drawdown')

ax.legend(frameon=False, loc='upper right')

plt.tight_layout()

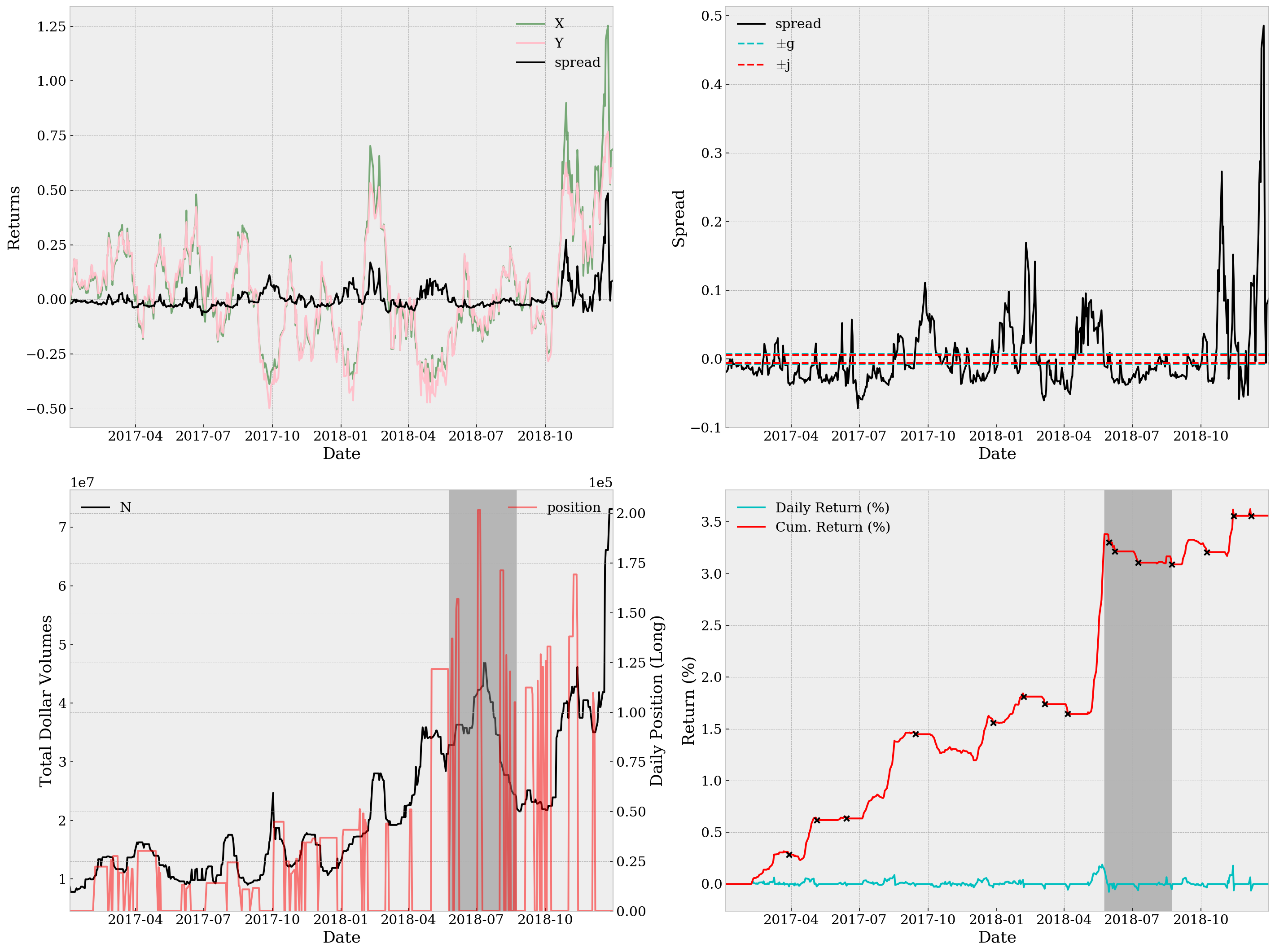

Using the parameters from Record 3, we run backtest against the test set, i.e. from 2016-12-02 to 2018-12-31. The plots are as below.

be = BacktestEngine('DRIP', 'XOP', start_date='2016-12-02', end_date='2018-12-31', ratio=-3)

st, sr, md, rt = be.run(M=20, g=0.007, j= 0.006, s=0.05000, verbose=True)

print('Sortino Ratio={:.4f}, Sharpe Ratio={:.4f}, Maximum Drawdown={:.4g}, YoY Return={:.2%}'

.format(st, sr, md ,rt))

Sortino Ratio=0.7407, Sharpe Ratio=0.2447, Maximum Drawdown=2.005e-11, YoY Return=1.76%

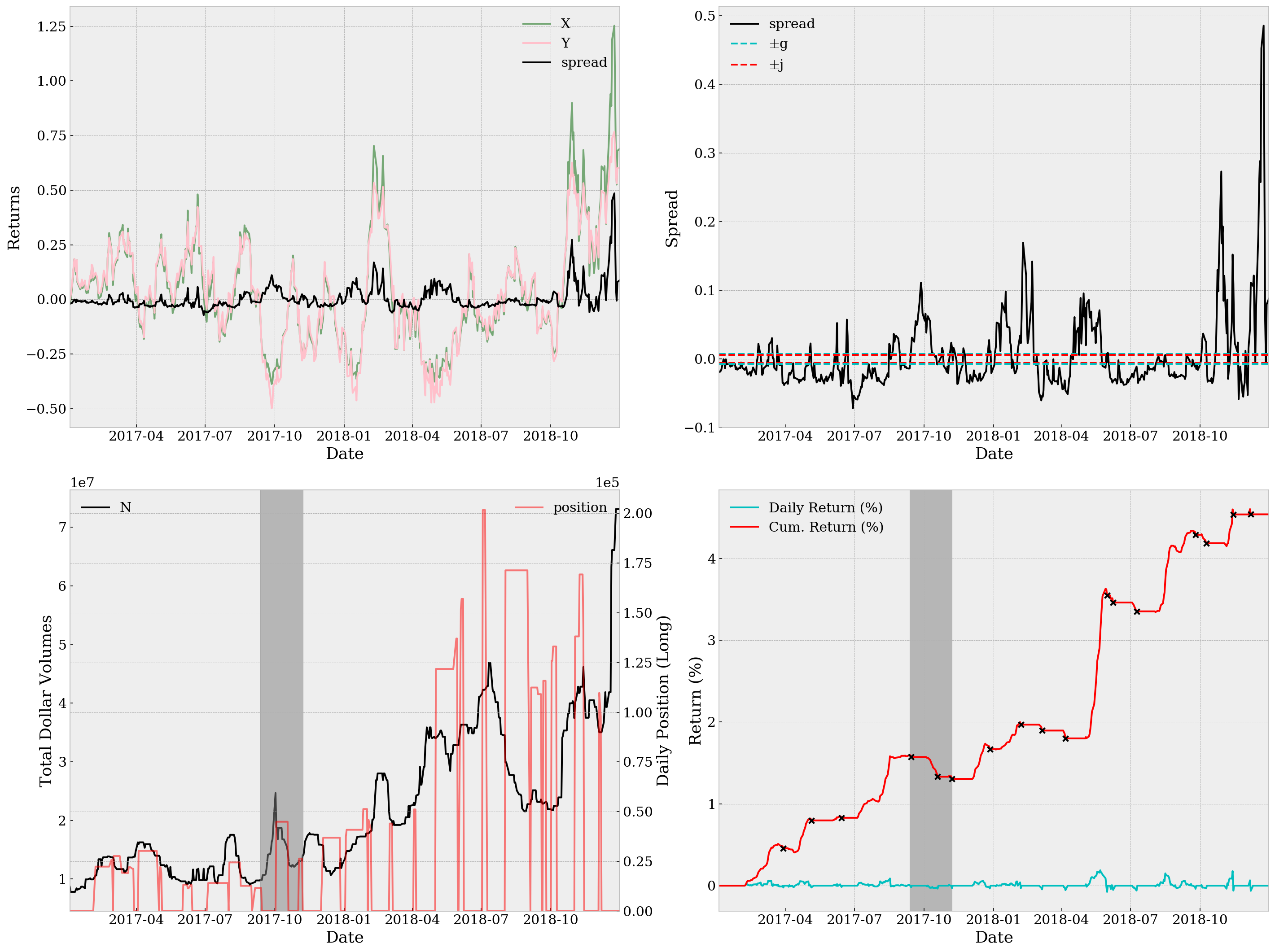

Using the parameters from Record 3, the backtest result is as below.

be = BacktestEngine('DRIP', 'XOP', start_date='2016-12-02', end_date='2018-12-31', ratio=-3)

st, sr, md, rt = be.run(M=20, g=0.007, j=-0.006, s=0.05000, verbose=True)

print('Sortino Ratio={:.4f}, Sharpe Ratio={:.4f}, Maximum Drawdown={:.4g}, YoY Return={:.2%}'

.format(st, sr, md ,rt))

Sortino Ratio=0.9394, Sharpe Ratio=0.2872, Maximum Drawdown=1.997e-11, YoY Return=2.24%

Conclusion

Both results are amazingly great (especially compared with our result using random parameters before any tuning). Considering here we’re not utilizing any future data in backtest, the performance is satisfactory despite we’re neglecting a lot executional details in our analysis, like transaction costs and market impacts. There are also several comments on the processing of data:

- We are using the first

Mdays to calculate the rolling median ofN, which causes a loss in data. Perhaps we should useMdays of further previous historical data to make up this loss. - Thresholds change, over time. To be more specific, the “ideal” thresholds change all the time, partly due to market regime shifting and partly other unknown reasons. We may, therefore, never have the “best” parameters for trading. Should we go for a dynamic version of spread trading? I doubt so. But it’s worth thinking if there’s any remedy for this problem.